The Week in Breakingviews |

|

| |

|

The Week in Breakingviews |

|

| |

| Insights from Reuters global financial commentary team |

|

|

|

By Peter Thal Larsen, Global Editor

|

|

|

|

Welcome back! The ceasefire in the Strait of Hormuz ended, but financial markets shrugged. Investors are more focused on artificial intelligence. What else should we be thinking about? Email me with your suggestions. (If this newsletter was forwarded to you, sign up here to get it in your inbox for free.)

Note: Links in this newsletter require a Breakingviews subscription. Subscribe here for you or your team to get full access. |

|

|

Five things I learned from Breakingviews this week |

|

|

|

The interior of a data centre in Chertsey, Britain, November 6, 2025. REUTERS/Toby Melville |

The artificial intelligence boom remains the dominant topic in financial markets. Despite renewed hostilities in the Strait of Hormuz, investors are mainly motivated by the fear of missing out on the bonanza promised by AI chatbots, data centres, and chips. At the same time, more far-sighted money managers have started preparing for the moment when the AI trade goes into reverse. The trouble is that there are few reliable places to hide.

The obvious assets to avoid in a crash are U.S. technology stocks. The “Magnificent Seven” American firms make up about a third of the S&P 500 Index. But other sectors have also cashed in on the gold rush. Analysts expect the so-called hyperscalers – Alphabet, Amazon.com, Meta Platforms, Microsoft and Oracle – to collectively shell out $4.8 trillion on AI chips, buildings and energy facilities by 2030. This promised flood of cash has not just lifted chipmakers – the Philadelphia SE Semiconductor Index is up 83% this year – but propelled producers of capital goods, construction firms, and energy utilities.

Overseas markets offer less shelter than before. Emerging market stocks are even more tied to a handful of AI-enhanced firms: three Asian chip giants make up roughly 30% of MSCI’s emerging markets benchmark. (See The Indexes of Power.) Their fortunes are inseparable from Silicon Valley, as SK Hynix underscored with this week’s $26.5 billion Nasdaq share sale. Europe has fewer home-grown tech champions, but Morgan Stanley analysts calculate that its listed companies generate more than half their sales outside the continent.

|

|

|

|

Other asset classes are also infected with the AI bug. Hyperscalers are increasingly tapping corporate debt markets: The Bank of England reckons they issued bonds worth roughly $160 billion in the first half of the year – about 50% more than in the whole of 2025. Amazon this week raised another $25 billion. Meanwhile, AI’s thirst for capital has soaked into private credit funds, asset-backed lending, and securitisation markets.

An outbreak of AI austerity would therefore be felt everywhere. Investment booms propel economic activity for a while, before leading to economy-wide recessions when spending stops. A broad selloff in global stock markets would knock consumer confidence, reduce employment and squeeze spending, while exposing financial weaknesses in other industries.

The fallout in part depends on what causes the bubble to pop. As I argued this week, analysts expect hyperscalers to roughly double their sales between 2025 and 2030 while simultaneously controlling capex. If corporate AI users prove slow to adopt the technology, cash flow forecasts will fall short. But even if AI usage catches on, a widespread switch to cheaper open-source or Chinese AI models could also leave the big U.S. firms high and dry. If this happens, investors are unlikely to dwell on the financial nuances. “When things break, the world will go into risk-off mode,” the head of one large pension fund told me this week. Good luck finding shelter.

|

|

|

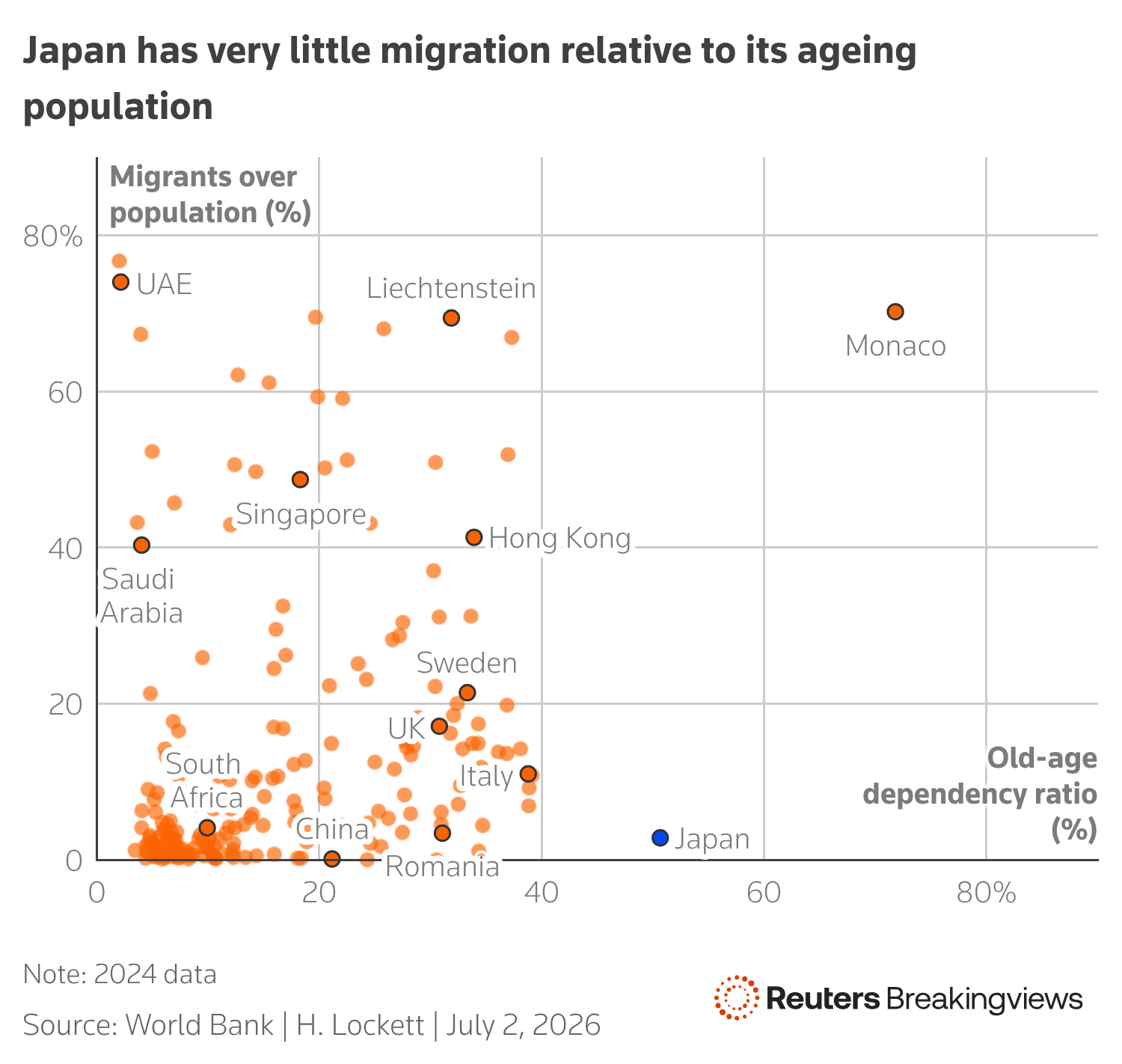

Japanese Prime Minister Sanae Takaichi wants to turbocharge growth and wages. But her bold economic plan suffers from a labour shortage. The country’s ageing population means its workforce is shrinking faster than any credible productivity boost could make up for. It is also unusual in having very few overseas workers. A better immigration policy is the answer, says Hudson Lockett.

|

|

|

|

|