With Wall Street futures back higher after the main indexes ended in the red for a second day on Wednesday, the readout for other chip-heavy global indexes from the Micron news was immediate. South Korea's KOSPI, whose most valuable firm SK Hynix filed for a U.S. stock offering of some $29 billion on Wednesday, jumped more than 5% on Thursday.

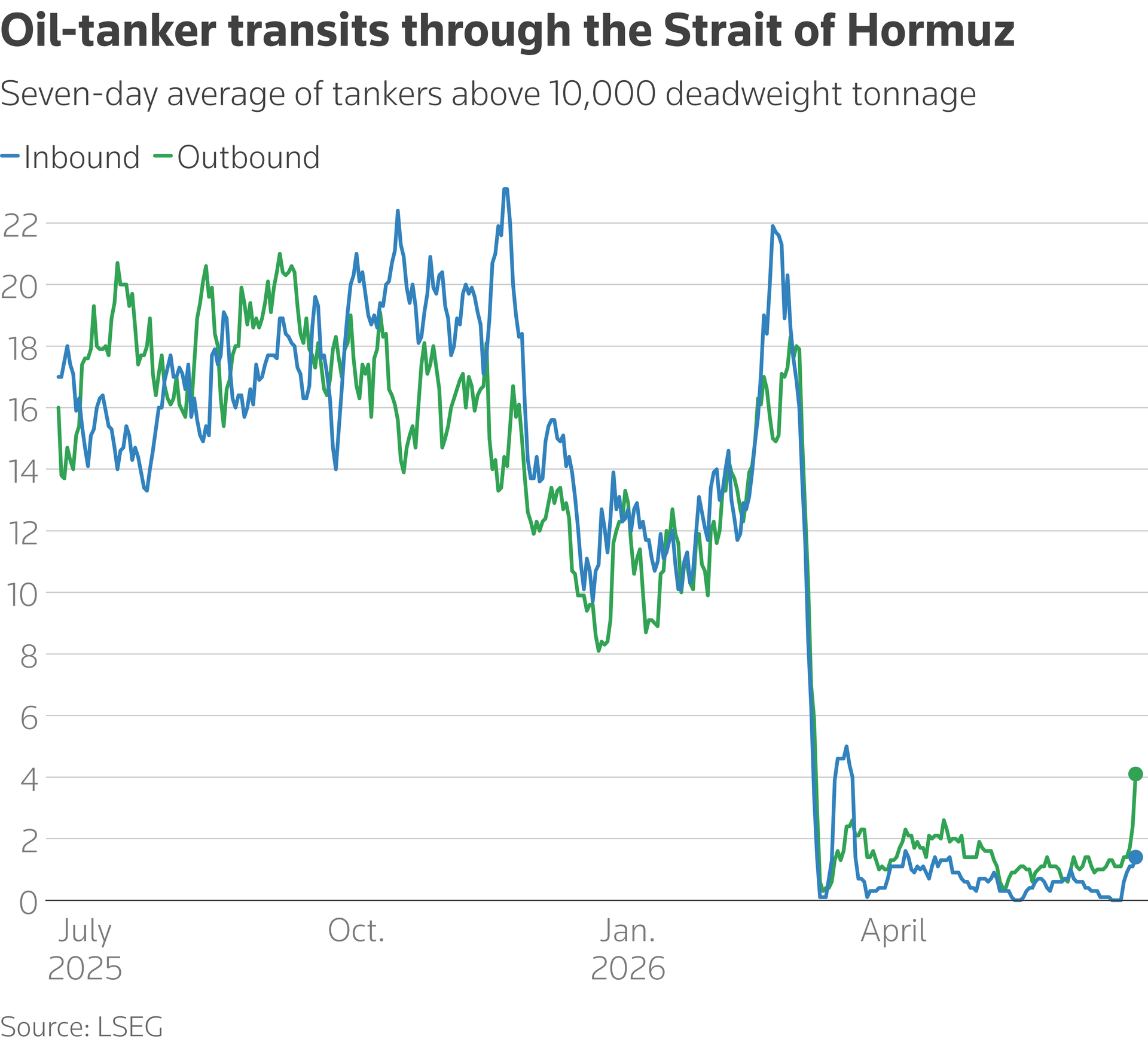

The other big milestone of the day was the return of global crude oil prices to levels seen just before the Iran war started in late February, with Brent crude now trading at under $73 per barrel. Energy prices' completion of this dramatic four-month round trip came amid more reports of rising shipping traffic in the Strait of Hormuz since the announcement of the U.S.-Iran interim agreement.

While that, and some poor U.S. housing data, weighed on long-dated Treasury yields, it did little to defuse Federal Reserve rate-hike expectations. Two-year Treasury yields did slip but remain some 75 basis points higher than they were just before the Iran war.

That's partly because core U.S. inflation was a problem even before the war started. We'll get an update on that later today with the release of the May U.S. PCE report. It's expected to show that core annual inflation ticked higher to 3.4% last month.

The Fed's wariness is also partly connected to expectations that the AI spending surge, soaring stocks and rising chip prices could be amplifying inflation more broadly, an issue that could - perhaps ironically - be worsened if the fuel price retreat takes the brakes off economic activity and spending elsewhere in the economy.

With that, onto today's column.