Evening Briefing: Europe

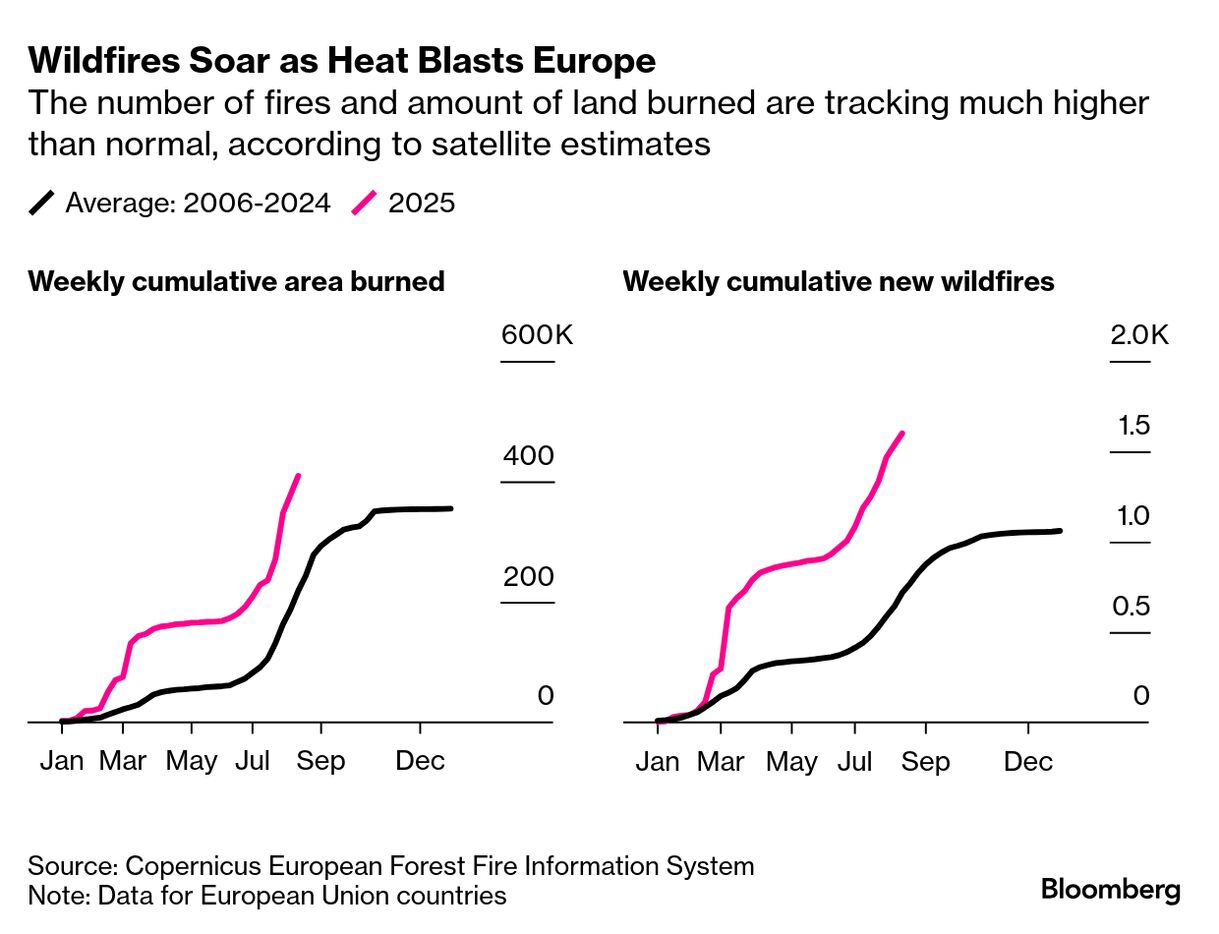

| Bloomberg Evening Briefing Europe | | | | Vladimir Putin announced before his meeting with Donald Trump in Alaska on Friday that Russia and the US can now begin to work on a a new arms control treaty. The Kremlin leader suspended participation in the New Strategic Arms Reduction Treaty, or New START, in 2023. Russian Security Council Secretary Sergei Shoigu subsequently said negotiations on a new accord would have to cover issues including NATO expansion, any US global missile-defense system and the deployment of ground-based missiles.  Rescuers work at the site of a Russian strike on a nine-story residential building in Kyiv on July 31. At least seven people were killed and dozens more were injured, as Russia launched a countrywide attack with drones and missile, local authorities said. Photographer: Sergey Dolzhenko/Shutterstock Editorial Putin’s statement today comes after Trump threatened “very severe consequences” if the Russian president didn’t agree to a ceasefire in Ukraine. The US president later backpedaled on expectations for the Alaska meeting. Ukrainian leader Volodymyr Zelenskiy, excluded from the summit, has warned Trump that Putin is “bluffing” and has no intention of ending his war. (Russia recently made a series of battlefield advances in Ukraine.) Trump said he hoped to book a “quick second meeting” with Zelenskiy, who is in London as the guest of UK Prime Minister Keir Starmer. Still, US allies in Europe have expressed concern about the potential for unilateral terms coming out of the summit—terms that would disadvantage Ukraine and undermine Europe’s safety. There are also worries Russia might insist on Ukraine conceding territory to make a deal, including the Donbas as well as Crimea, which was illegally annexed in 2014. Ukraine has rejected ceding territory to Russia, which over 11 years has killed tens of thousands of Ukrainians, flattened cities and towns and been accused of committing scores of war crimes. –Helen Chandler-Wilde | | What You Need to Know Today | | | Deadly fires in Greece and Spain have led to thousands of people being evacuated, with a wildfire still burning in an inaccessible part of Chios, causing a blackout across the island. Europe has been seriously affected by fires recently, as four major heat waves have dried out the ground and baked vegetation. On top of that, this week has seen strong winds which have quickly spread flames. Nearly 4,400 square kilometers (1,700 square miles) have burned so far this year, with the European Union experiencing 16 wildfire events—already the same number as in the entire fire season of May to October last year. | |

| | Turkey’s central bank kept its year-end inflation forecast of 24% unchanged, the same prediction it had in May—striking a more optimistic tone than either markets or business after annual consumer inflation hit 33.5% last month. The bank’s quarterly inflation report is closely watched by investors, who try to gauge future interest rate decisions from them. Governor Fatih Karahan today said that the bank was “absolutely not on autopilot” with cuts, and said that given inflation is still above forecasts, a “tight and determined stance” is still needed. In the release, the bank upped their predictions for 2026 from 12% to 16%—but stuck to their long term aim of bringing inflation down to 5%. | |

| | The super-rich exodus from the UK after changes to tax rules is broadly in line with expectations that one in four with trusts would leave, according to the Financial Times. The numbers could offer respite for Chancellor of the Exchequer Rachel Reeves, whose “tax the rich” policy caused criticism from people fearing that wealthy people would flee and leave a hole in the nation’s finances. Other news the Labour government may find cheering includes above-expectation growth figures released today, which put the UK at the top of the G-7.  Rachel Reeves Photographer: Carl Court/Getty Images Europe | |

| | Return to office mandates in banks are happening at a faster rate in North America than in Europe. Five years after the Covid pandemic began, just seven out of the 15 most valuable banks in Europe have asked all or some of their staff to come to the office four or more days a week, according to Bloomberg analysis. In the US and Canada, that’s 11 out of 15. In the group of European banks, the average requirement is 3.4 days a week in the office—but 4.2 days in the North American group. | | | |

| | Israel is planning to expand its settlements into the E1 area of the West Bank, which would effectively bisect the enclave and “bur[y] the idea of a Palestinian state,” according to Israel’s finance minister. Over the past year, and in the face of global condemnation as a violation of international law, Israel’s far-right government gave the green light to a large increase in settlement building in the Palestinian territory. The West Bank-based administration of Palestinian Authority President Mahmoud Abbas condemned the announcement. Along with the devastation in Gaza and recurrent violence by some settlers against Palestinians, it “will only lead to further escalation, tension and instability,” said Abbas spokesperson Nabil Abu Rudeineh. | |  Israel Finance Minister Bezalel Smotrich holds a map of an area near the settlement of Ma’ale Adumim, outside Jerusalem on Aug. 14 Photographer: Menahem Kahana/Getty Images | |

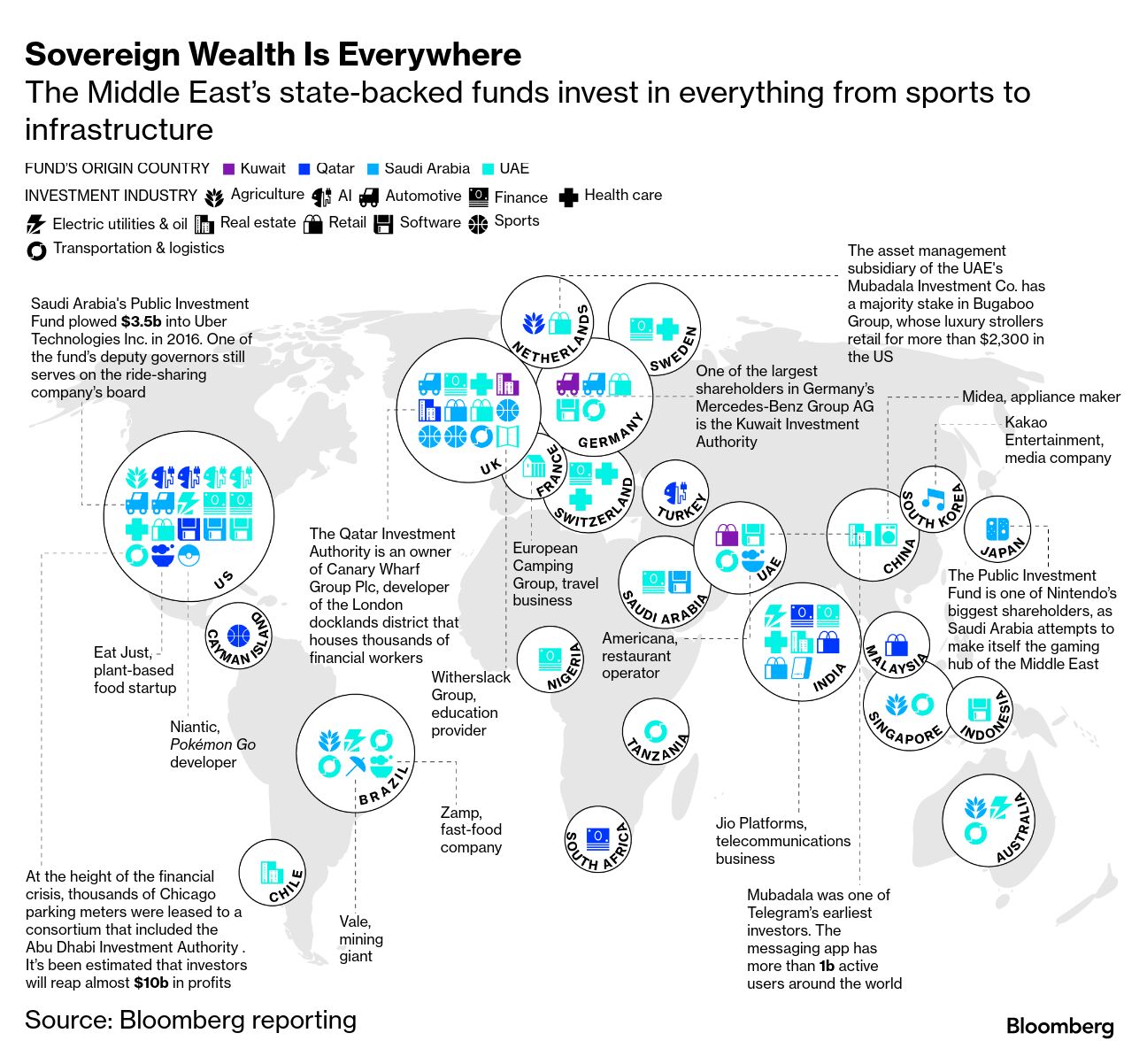

| | Business confidence in the Middle East remains high even as conflict escalates, with billions of dollars flowing in and out of Qatar, Saudi Arabia, Abu Dhabi and Dubai despite Iran launching missiles at a US air base in the region this summer in retaliation for a surprise American bombing raid. Low tax regimes and $5 trillion of family and sovereign wealth has allowed the region to weather instability and remain open for business—with Riyadh working on deals including BlackRock landing a $5 billion investment pledge and talks with Elon Musk’s xAI. | |

| | Viktor Orban’s grip on power in Hungary may be slipping, as a vision of making the country the electric-vehicle capital of Europe has not gone as planned. The city of Debrecen—which was at the heart of this strategy as well as being a stronghold of the authoritarian leader—has seen more than $10 billion of foreign investment in recent years, with new plants for BMW and CATL. Yet the mood has changed as Europe’s EV industry has struggled, with Hungary on the edge of a recession in the first half of the year and protests springing up in Debrecen.  Peter Magyar, leader of opposition party Tisza, holds a townhall meeting near the CATL battery plant in Debrecen last month. Photograph: Bloomberg | | What You’ll Need to Know Tomorrow | | | | |