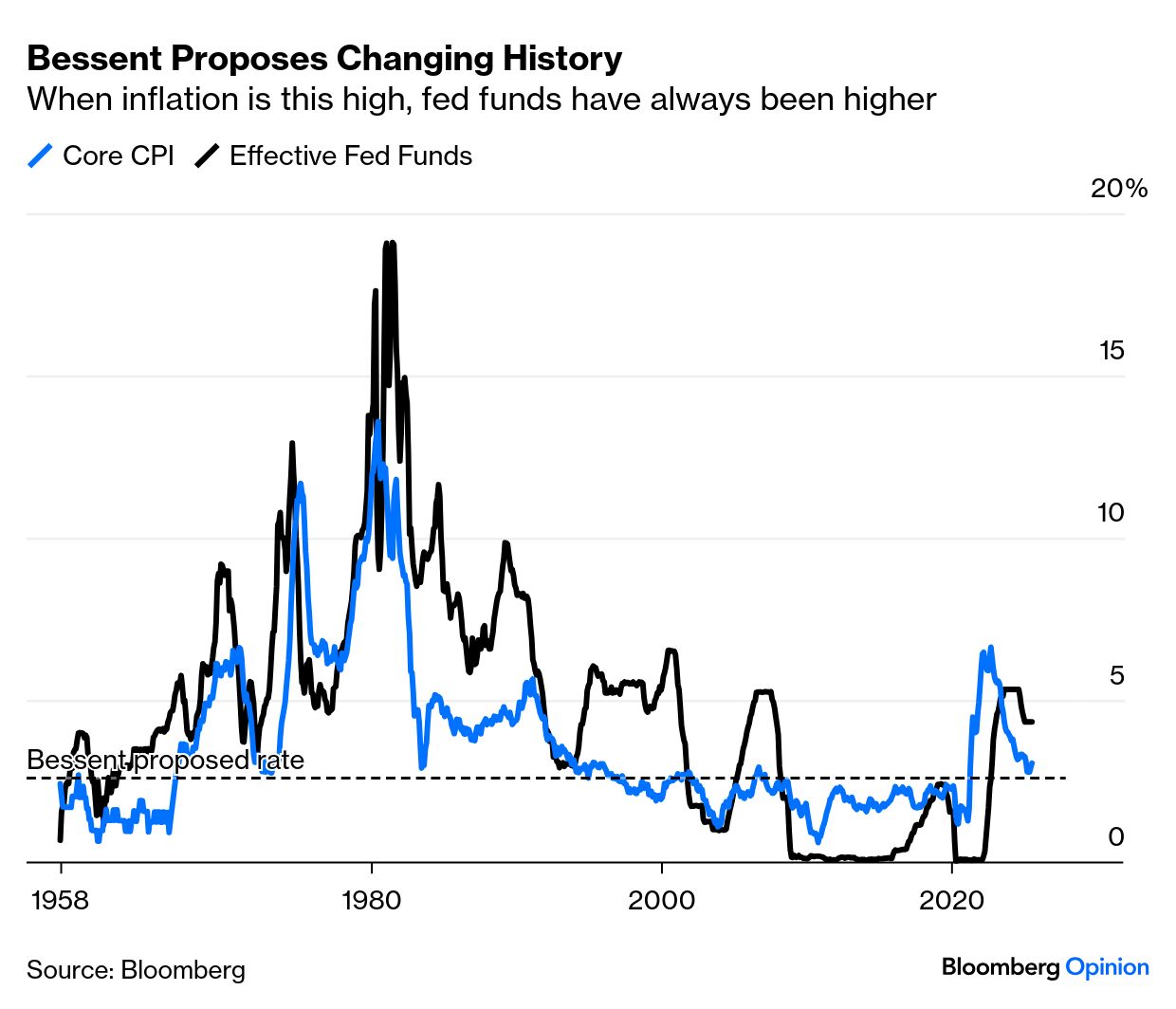

| Scott Bessent, the US Treasury secretary, made big news on Blooomberg Surveillance. He told the televised audience that “if you look at any model” for the fed funds rate, it suggests that “we should probably be 150, 175 basis points lower.”

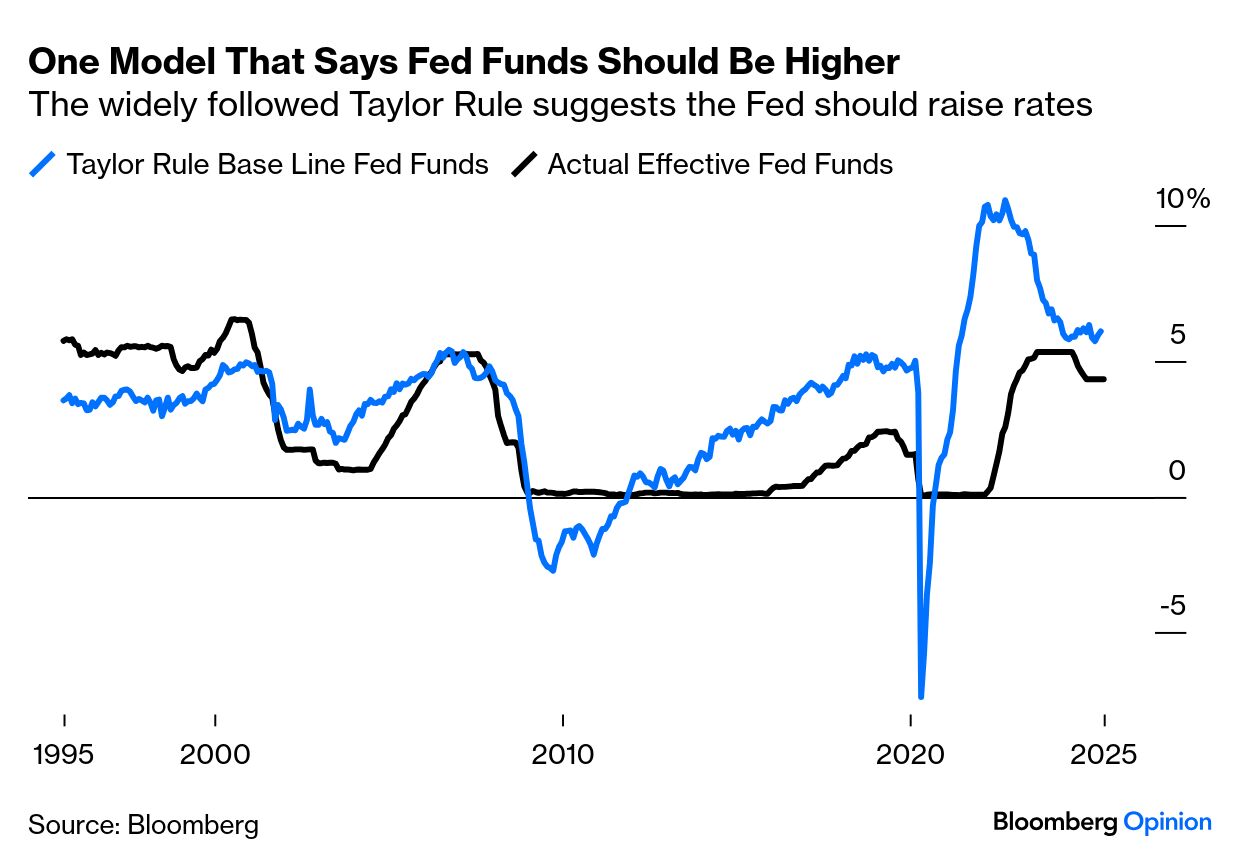

This is breathtaking. With the current effective fed funds rate at 4.33%, he is suggesting that it should be about 2.6%. Over the last 70 years, the rate has never been that low with inflation as high as it currently (with the core reading above 3%). So apparently “any” model now shows that US monetary policy has been misguided throughout that entire period and needs to be changed: In fact, it's easy to find a model that says fed funds should be far higher than 4.33%. Arguably the most famous is the Taylor Rule, named for John Taylor, a Stanford economist and former senior Treasury official who was a candidate for the Federal Reserve chairmanship eight years ago. His formula suggests the next move should be up:

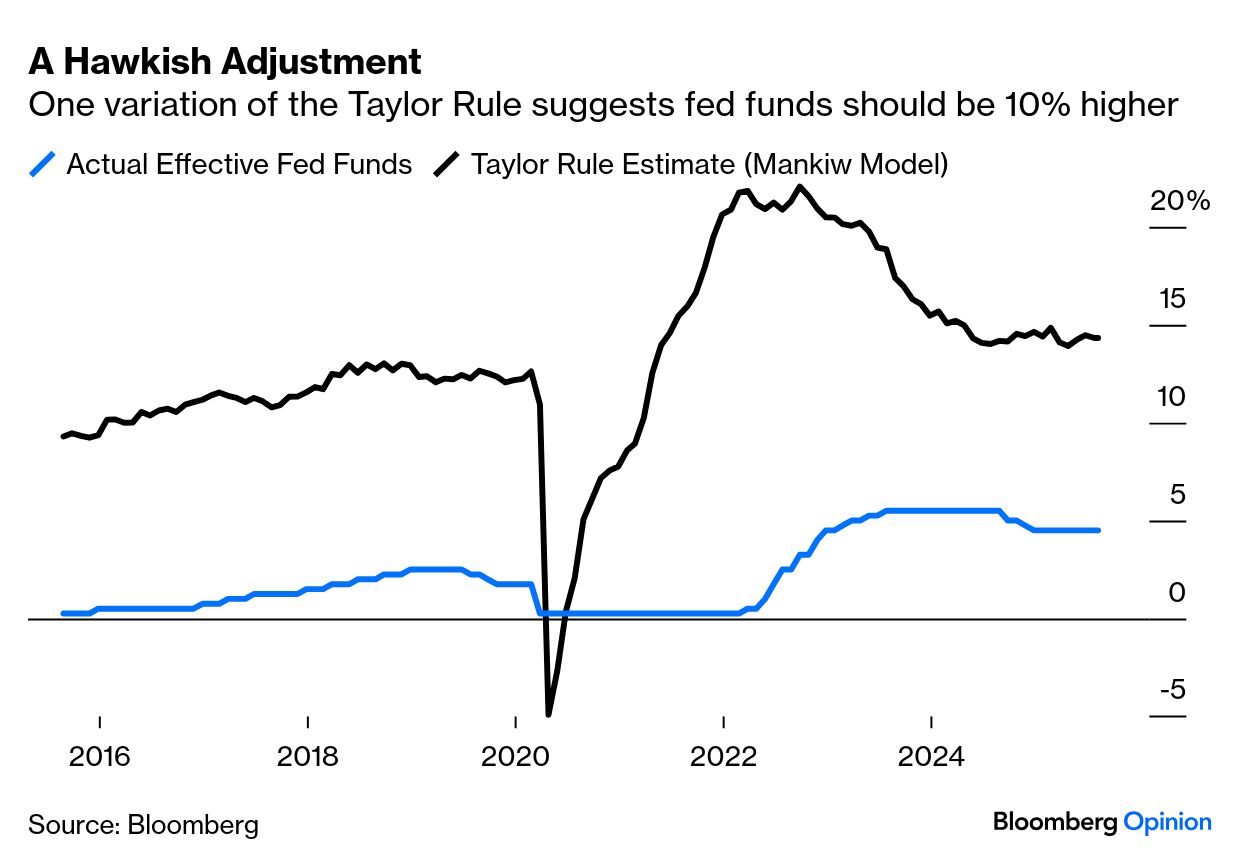

This is available on the Bloomberg terminal; it’s not exactly obscure. We also handily provide various different versions of the Taylor framework. This is the fed funds rate under the adaptation made by Gregory Mankiw, the Harvard economist who served as George W. Bush’s chairman of the Council of Economic Advisers:

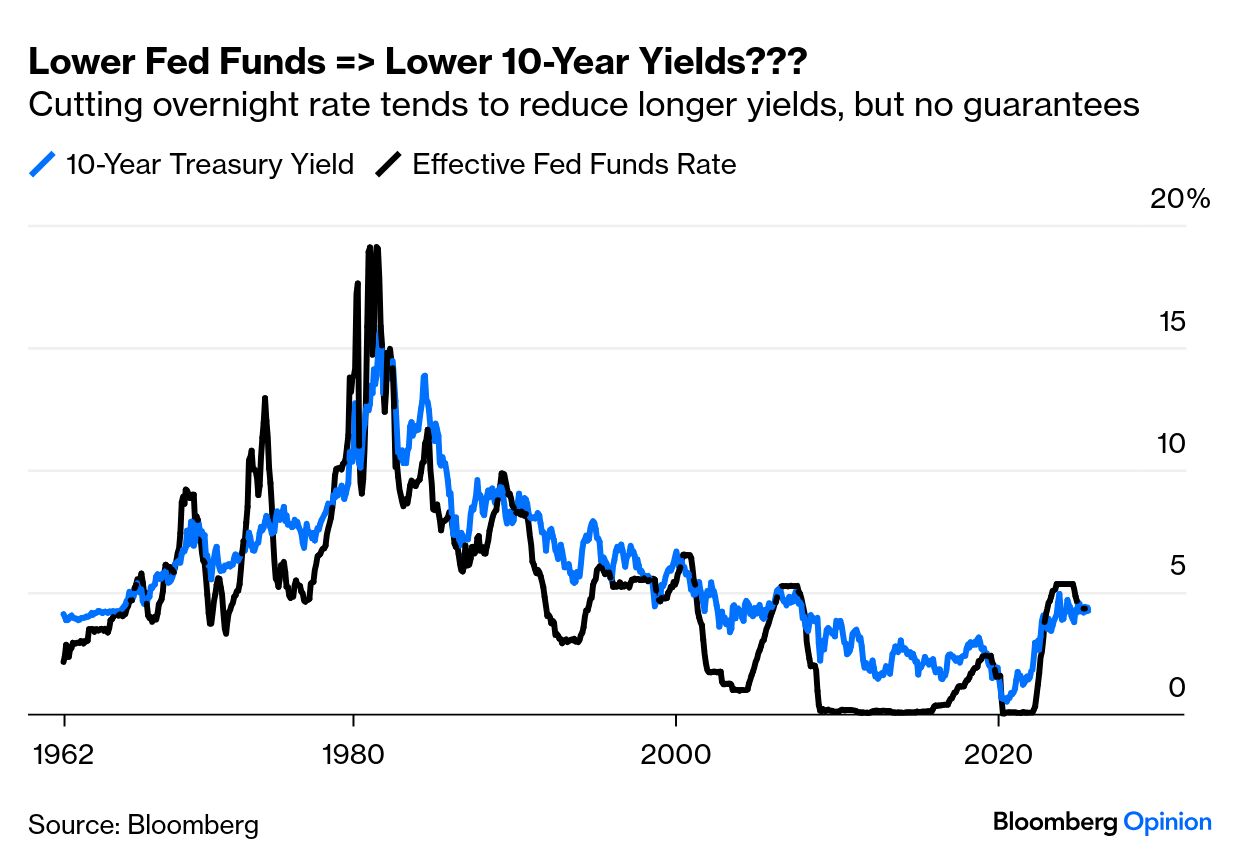

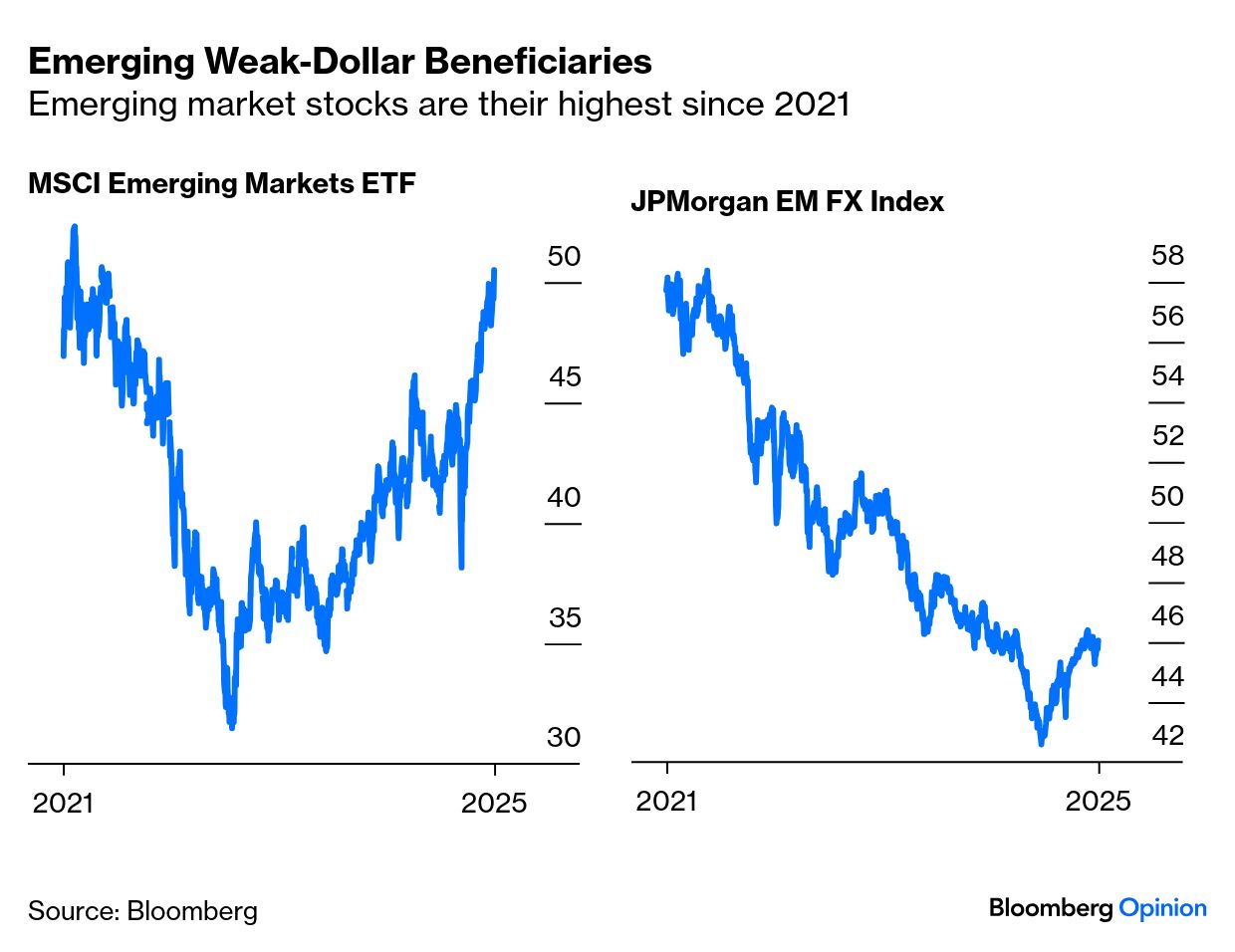

The point is not that these models are necessarily right. They may well not be. And Bessent has a right to express his opinion. But it’s absurd to suggest that “any” model would call for fed funds to be so much lower, and alarming to hear it from the US Treasury secretary. The bottom line we already knew from presidential social media accounts: Donald Trump wants lower interest rates, and more control over them. Fed independence has long been contested, and other presidents have kicked against it — but since the end of the gold standard in 1971, an independent Fed has been central to maintaining the dollar as the linchpin of the global economy. This is a dangerous game. Further, the drawback of allowing the Treasury Department to control both fiscal and monetary policy is that it can then coordinate them to rhyme with the political cycle. In the UK, finance ministers set base rates until 1997, creating a pronounced “stop-go” effect as governments pumped up the economy ahead of an election, and put on the brakes once they’d been reelected. This is miserable economics, as the UK’s weak postwar growth demonstrates, but decent politics. Even so, that implies that it’s madness for a government to behave like this six months into a four-year term. The likely outcome would be a short-term boom, and a pretty serious bust in time for the next election in 2028. So why all the pressure? The most obvious answer is to bring down longer Treasury yields, which determine the cost of servicing the government’s debt. All else equal, lower overnight rates from the Fed mean lower longer-term yields. But the Fed doesn’t control the long end. Last September’s jumbo fed funds cut was greeted by a rise in the 10-year yield. There have been many other incidents when Treasuries refused to follow the lead that the Fed set for them: The White House has also been clear that it wants a weaker dollar. The latest dose of pressure on the Fed appears to have achieved this, as the currency has fallen over the last few days. That’s helpful for many people, but particularly for the emerging markets, where stocks have at last taken out the high they made during excitement over China in early 2021: For now, the impact is clear as investors are persuaded that there is no recourse but to continue buying US stocks. The latest Markets Pulse survey of Bloomberg terminal users found 59% believing that pressure to lower interest rates would boost US stocks compared to peers — even though some 70% expect tariffs to have had a negative effect by the end of the Trump 2.0 term. The great majority were uncomfortable with the premium that US shares currently command — but leaning on the Fed has convinced many that the rate environment will get more conducive from here. |