| We’re in the unusual situation where fund managers almost uniformly say US stocks are overvalued, yet everyone is piling in. This disconnect, as the S&P 500 Index sets repeated all-time highs, is the market’s biggest vulnerability going forward.

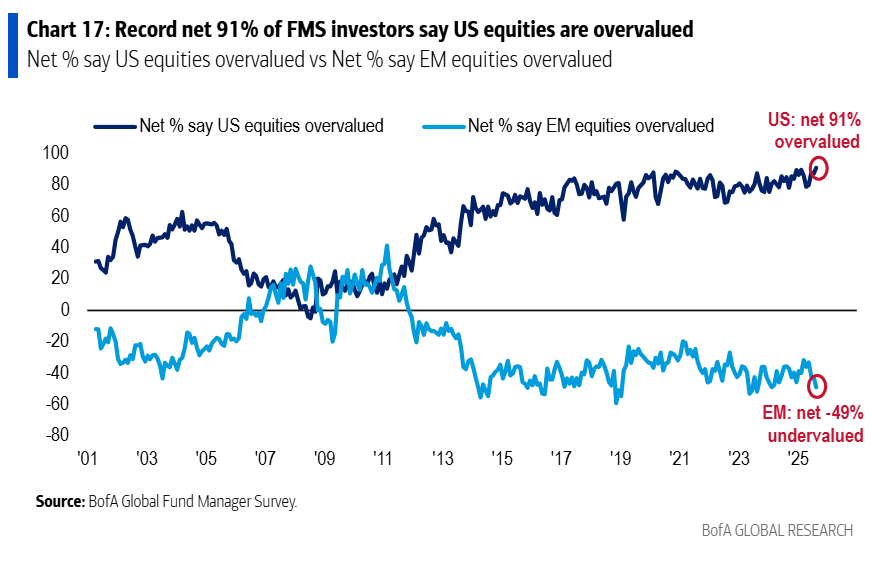

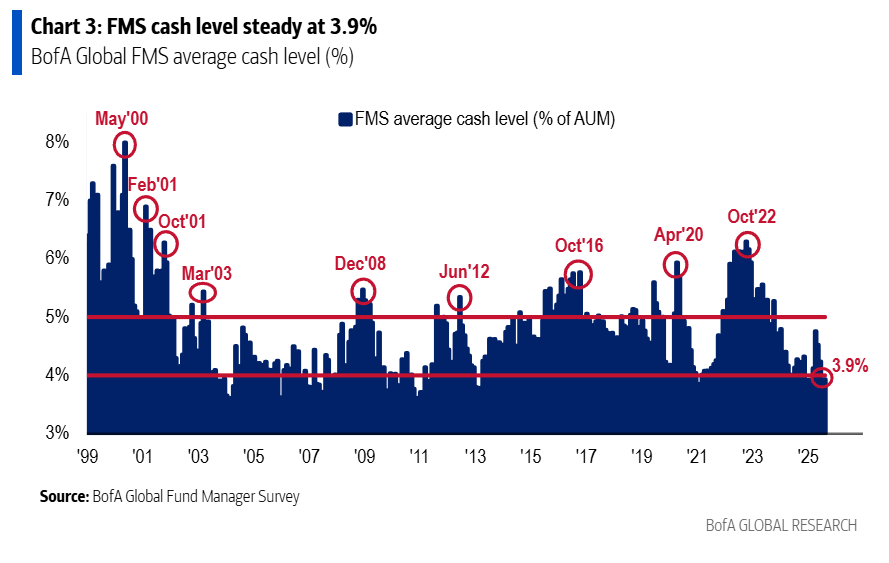

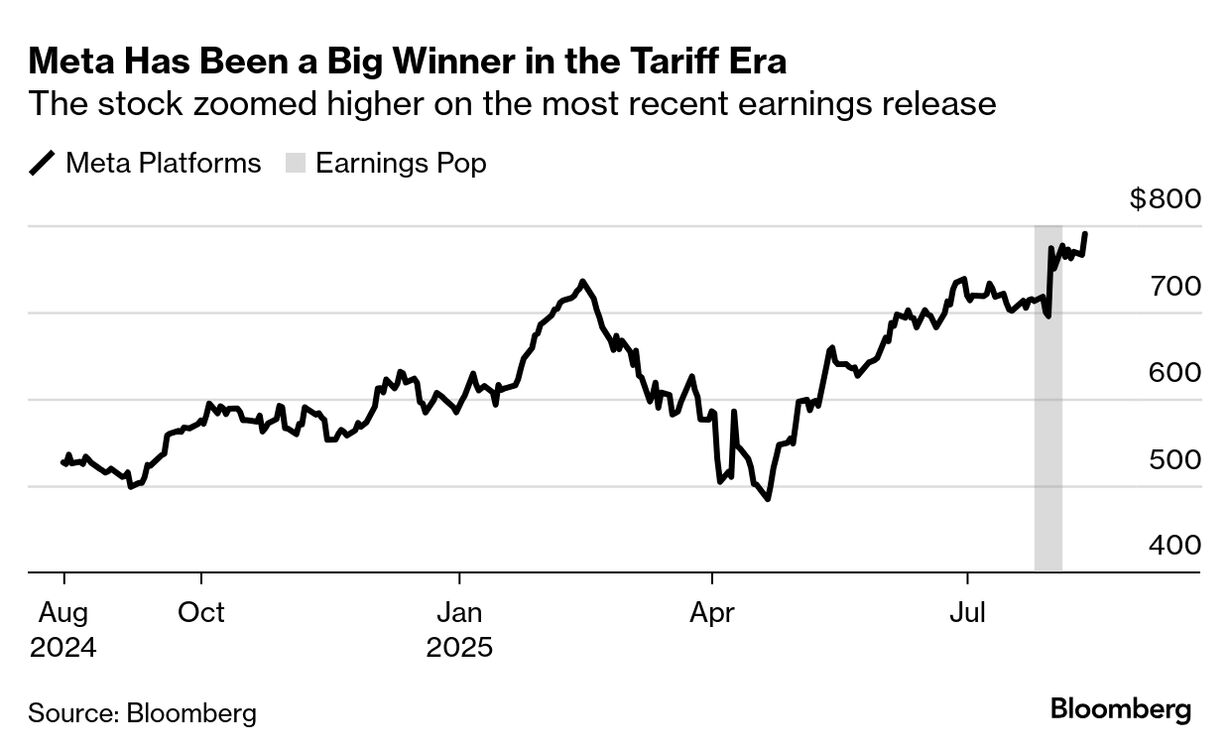

At the first sign of trouble — for example if tariffs do ultimately lift consumer prices and derail expectations for Federal Reserve interest-rate cuts -- they’re liable to sell. And it’s a risk the market may have to contend with in the next few months. To get a sense of the latest positioning, look at the most recent Bank of America Global Fund Survey results. A record 91% of institutional investors say US equities are overvalued. But don’t watch what fund managers say, watch what they do, because they’re fully invested. Cash levels are near the bottom of historical levels over the past quarter-century. BofA says investors increased allocation to emerging markets, global stocks and utilities given the valuations in the US. However, going long the so-called Magnificent Seven — i.e., megacap US technology shares — is the most-crowded thematic trade, the survey shows. Basically, institutional investors — cautious after President Donald Trump’s April 2 tariff announcement and slow to buy the dip amid recession fears — have lagged behind mom-and-pop investors who piled in when Trump delayed most of his tariffs in April. Big money managers are now playing catch-up, with BofA saying it just saw a near-record week of buying by institutional clients. That marked not only the 10th-largest flow into stocks in its data since 2008, but the flow into tech shares was in the 99th percentile, led by institutional buyers. This is extreme. It creates huge risks too if people are buying stuff they consider to be overvalued. Two things beyond chasing returns are driving this bull market. The first is the lack of an economic hit to the economy from tariffs and tariff uncertainty. The second is the strong earnings performance of megacap tech. In an economy still doing well, and given Big Tech’s weight in the indexes, investors are almost forced to buy in order to keep up with benchmarks -- especially if they tried to hedge or rotate into areas they considered less expensive. Take Meta Platforms Inc., for example. It’s not an obvious place to go to invest in artificial intelligence. Yet, of all the Magnificent Seven stocks, its earnings performance was the most surprising, with gains in ad spending offering a sign that tariffs have yet to hurt the US economy significantly. The stock surged when the company said it would invest heavily in artificial intelligence. Most of the other Magnificent Seven stocks that reported beat estimates. Tesla Inc. was an exception. Nvidia’s earnings, still ahead this month, should be stellar too. |