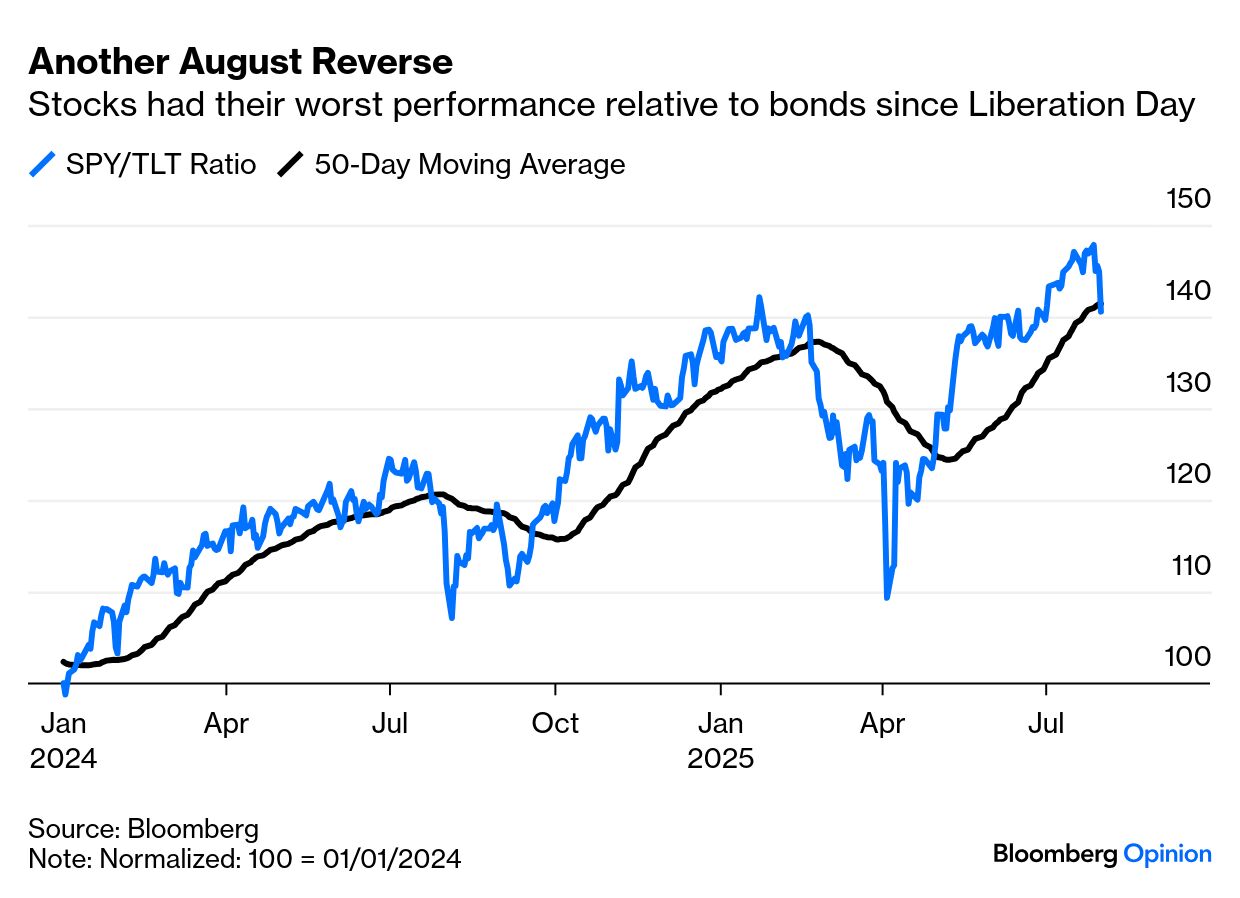

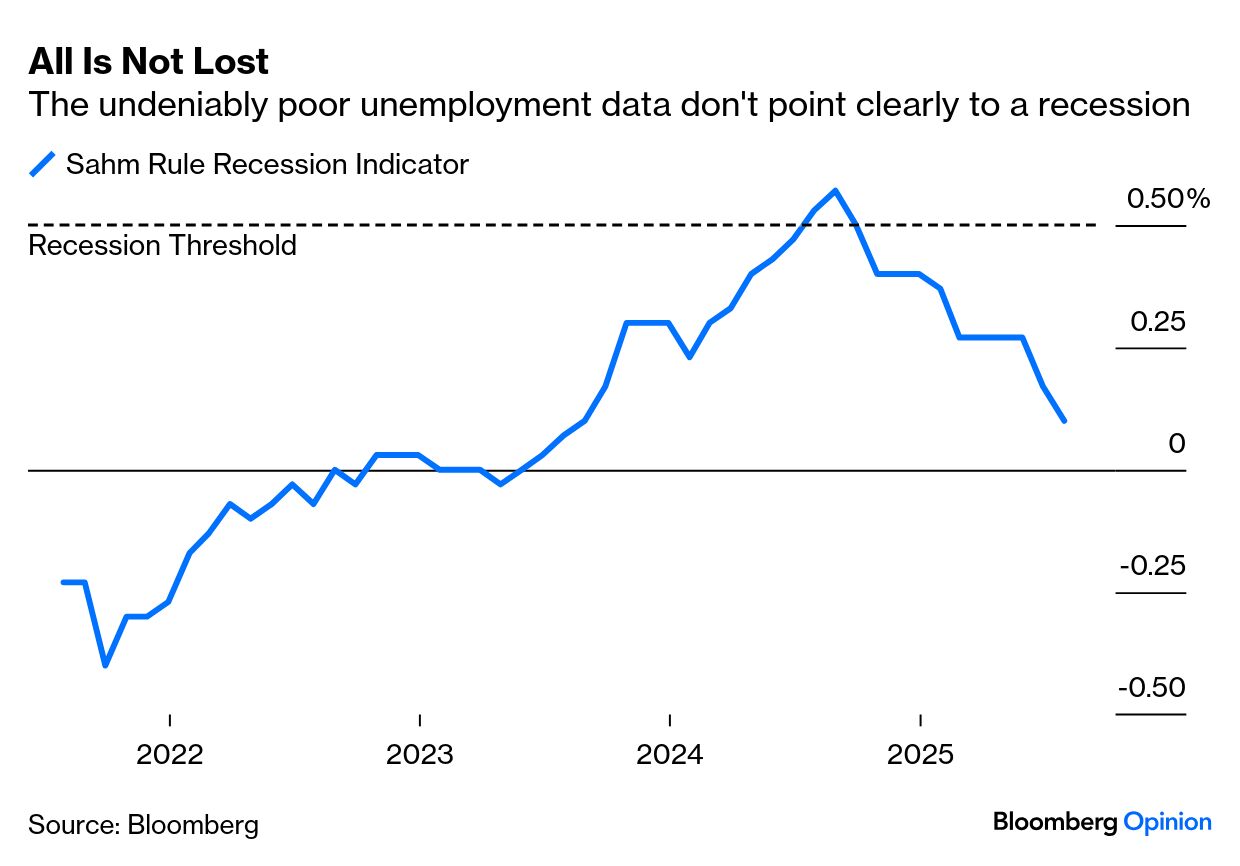

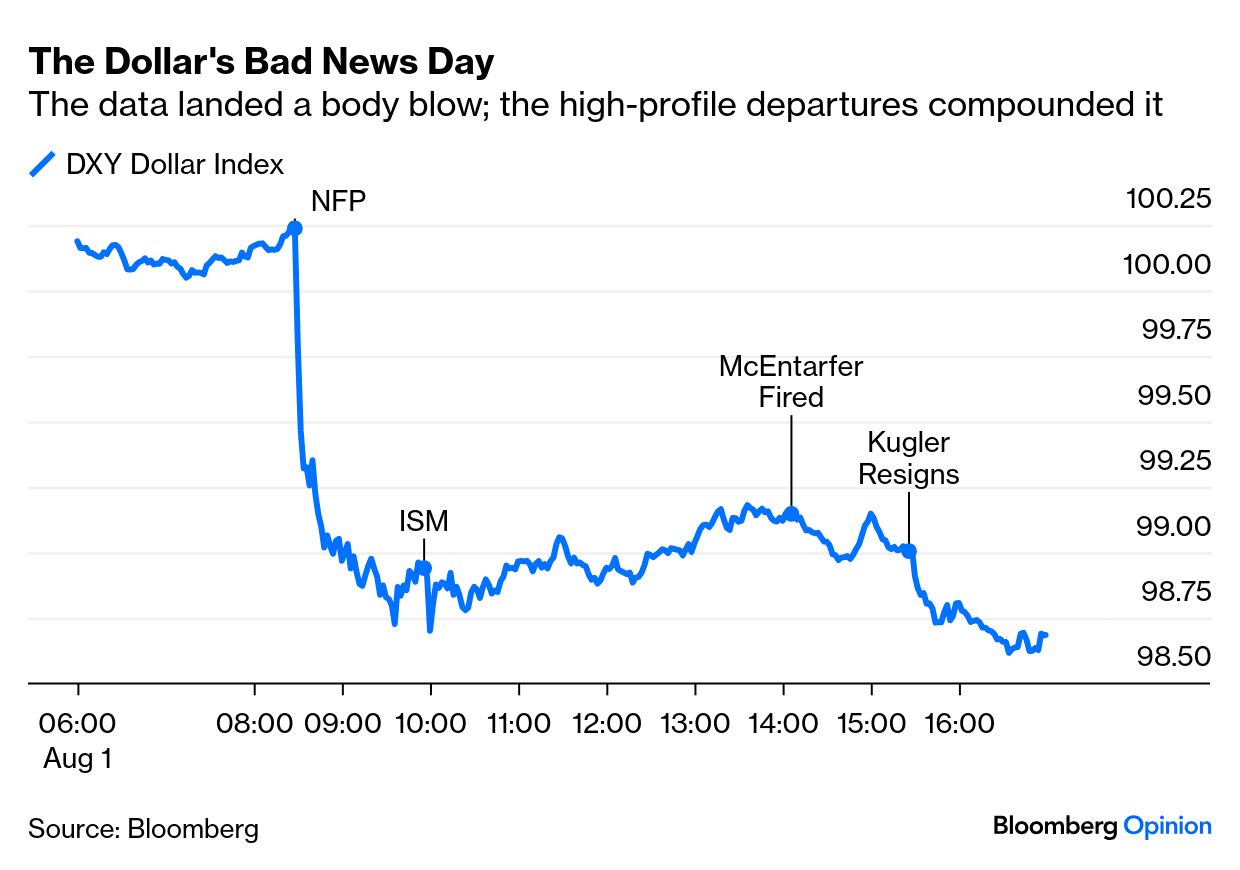

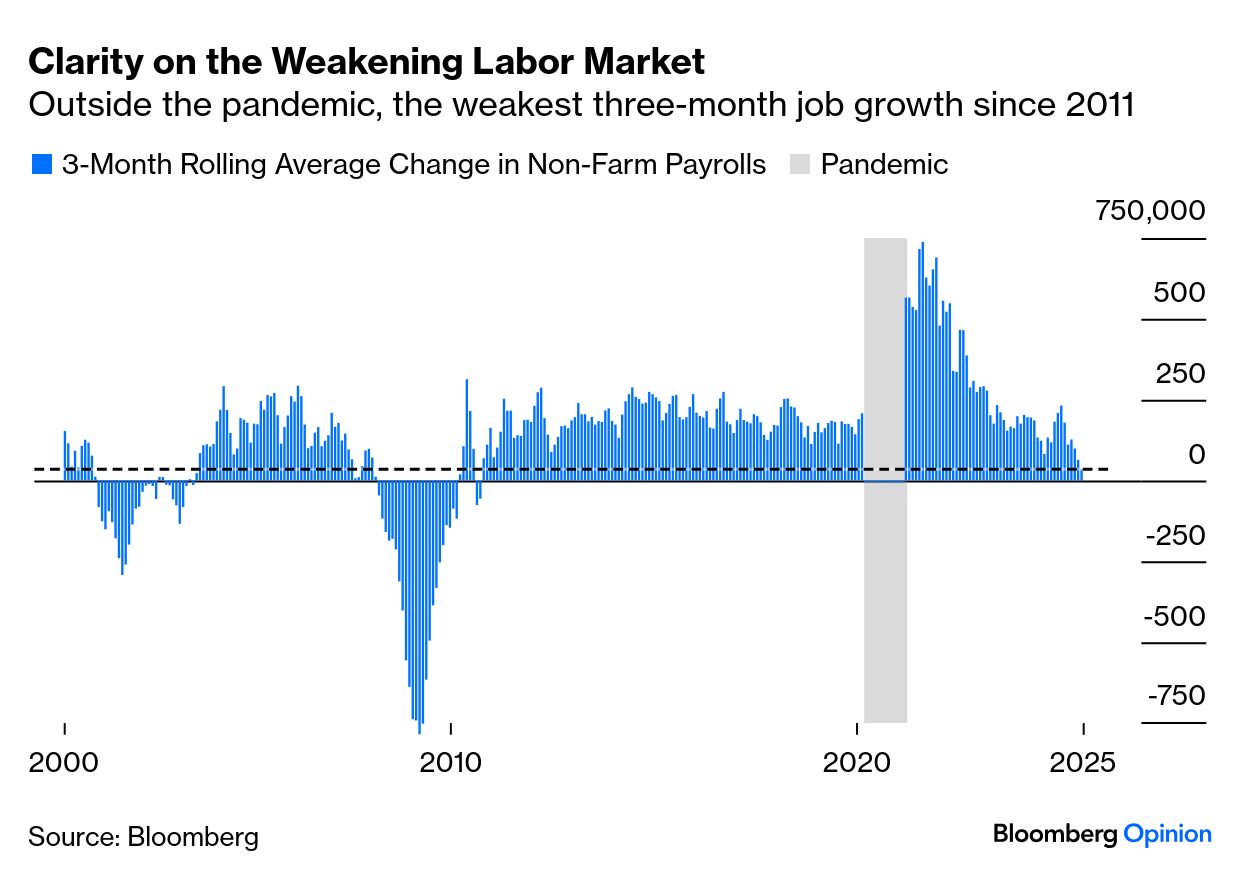

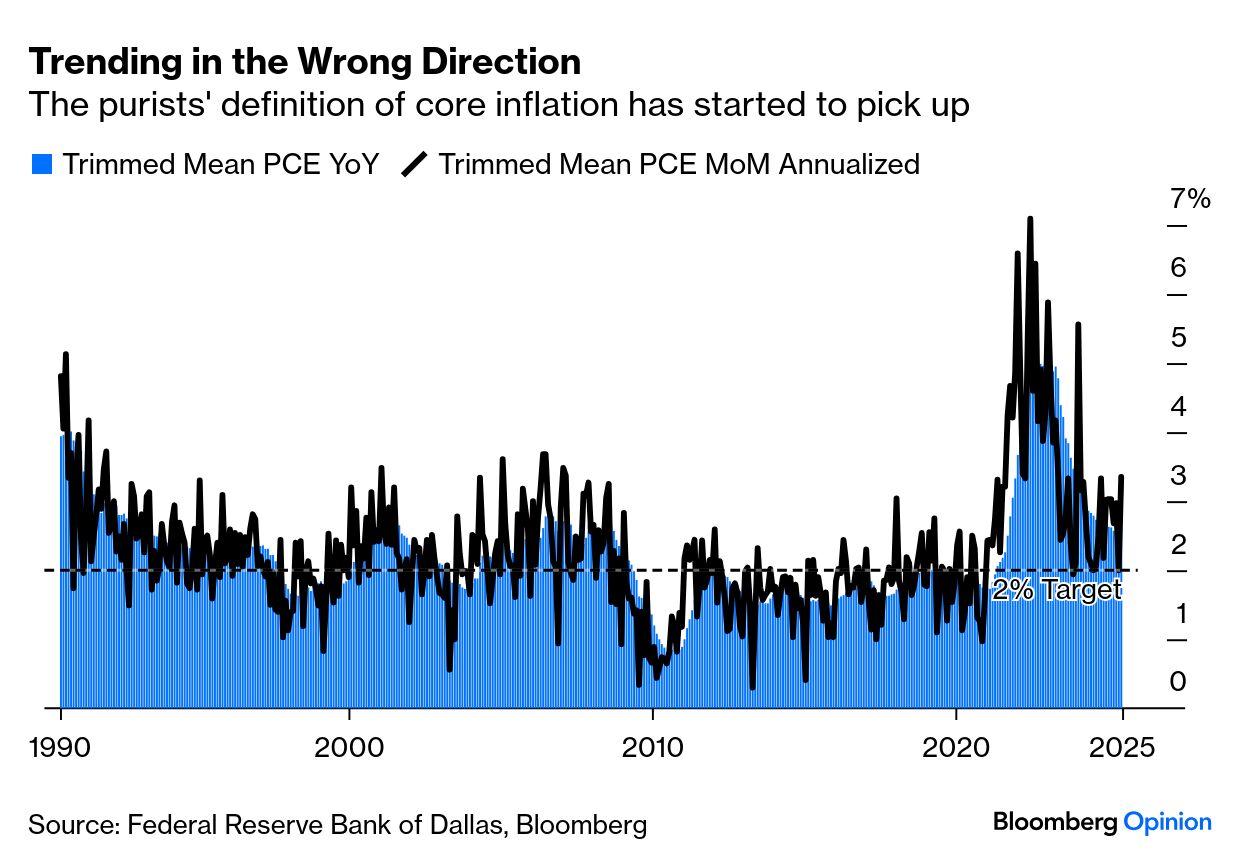

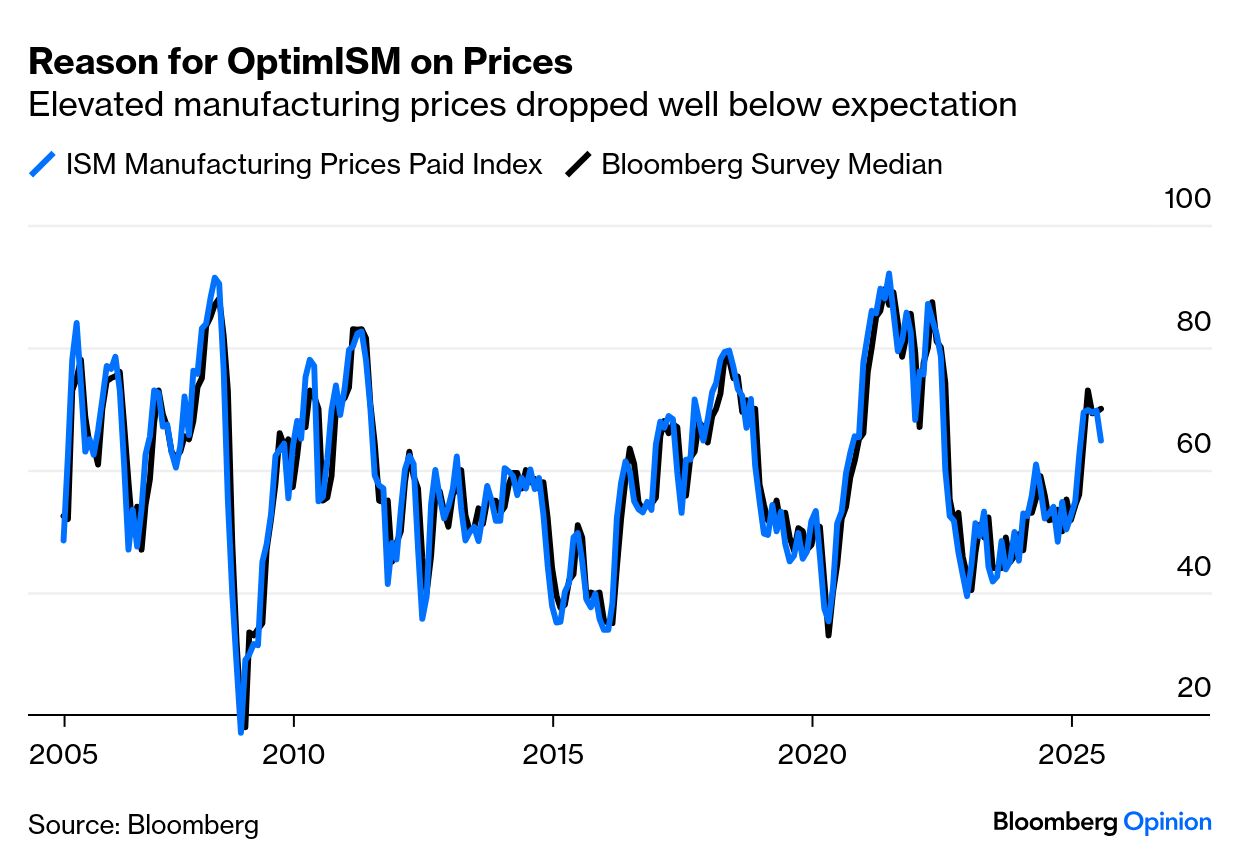

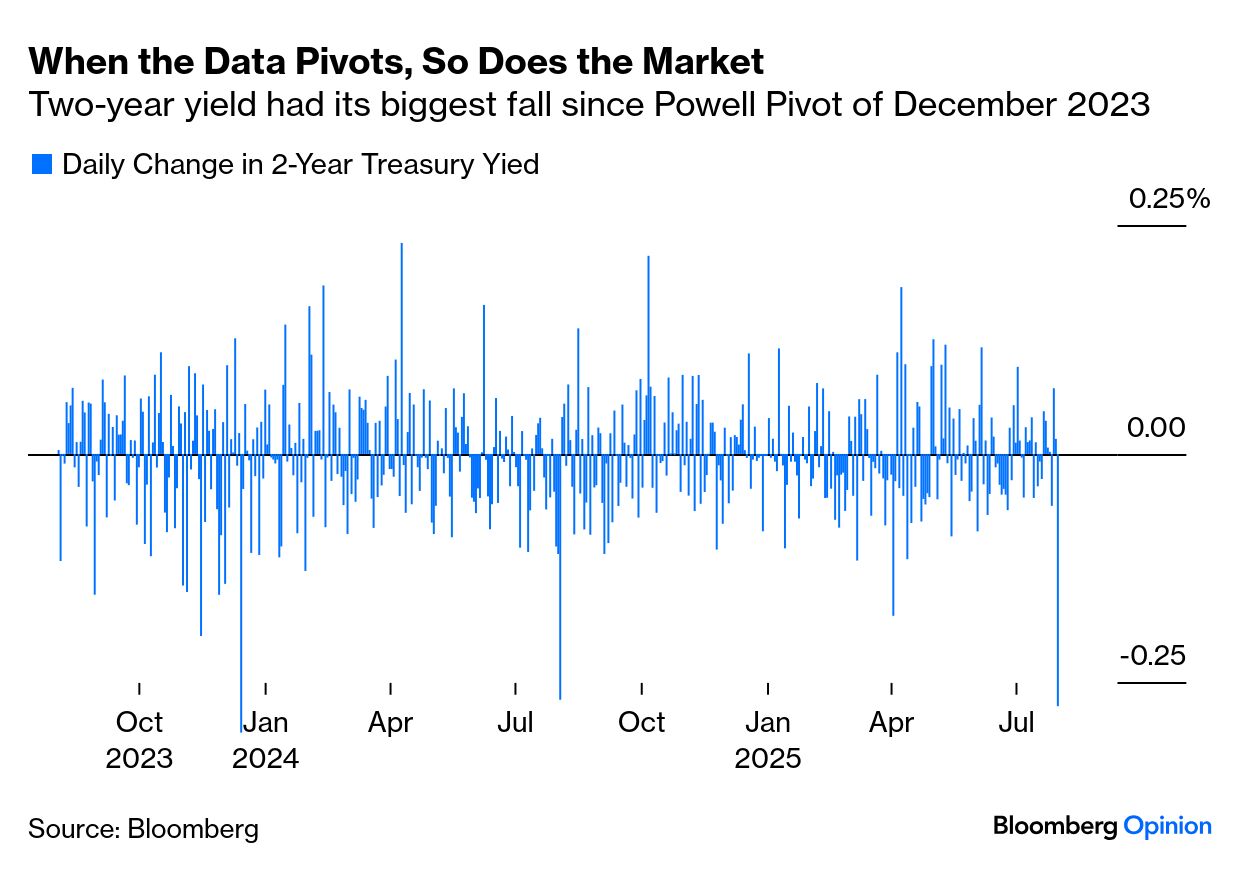

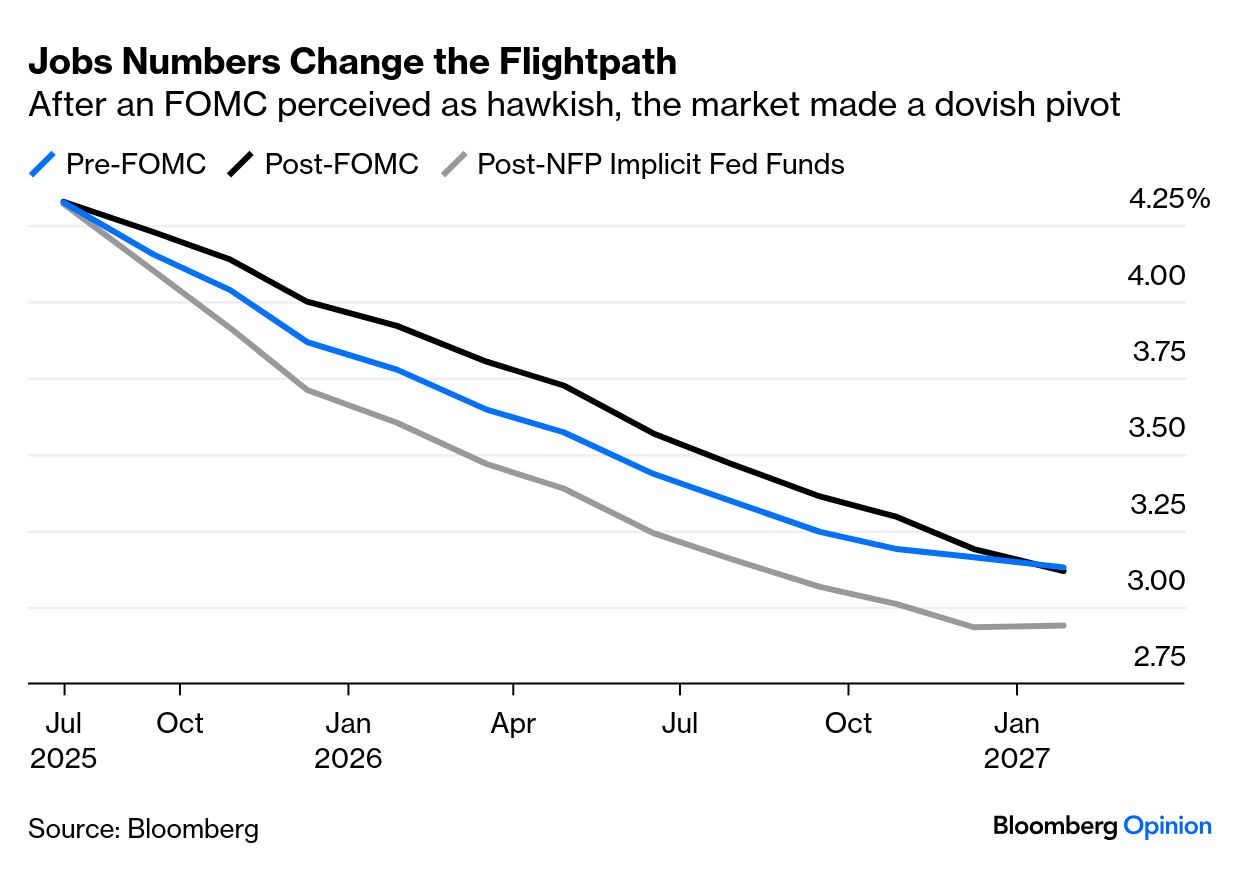

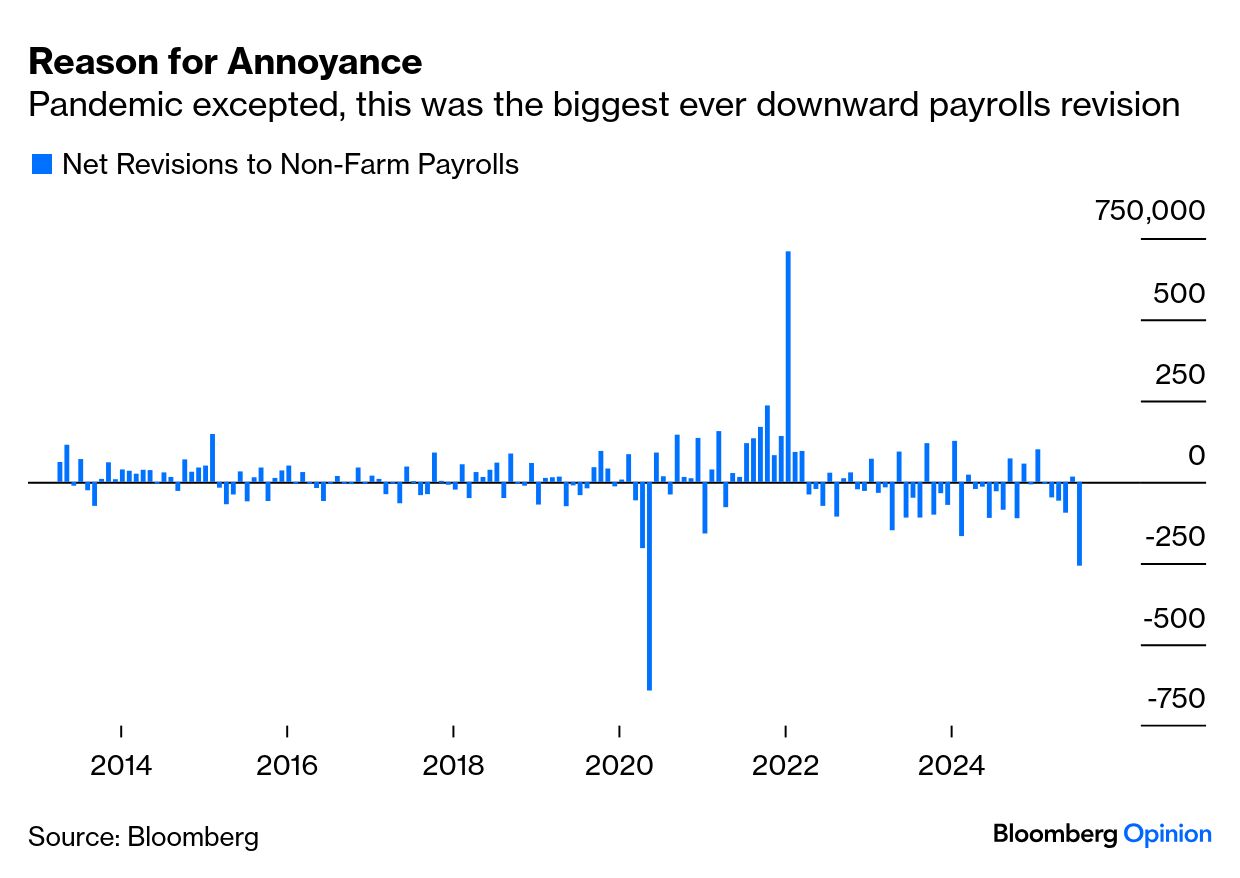

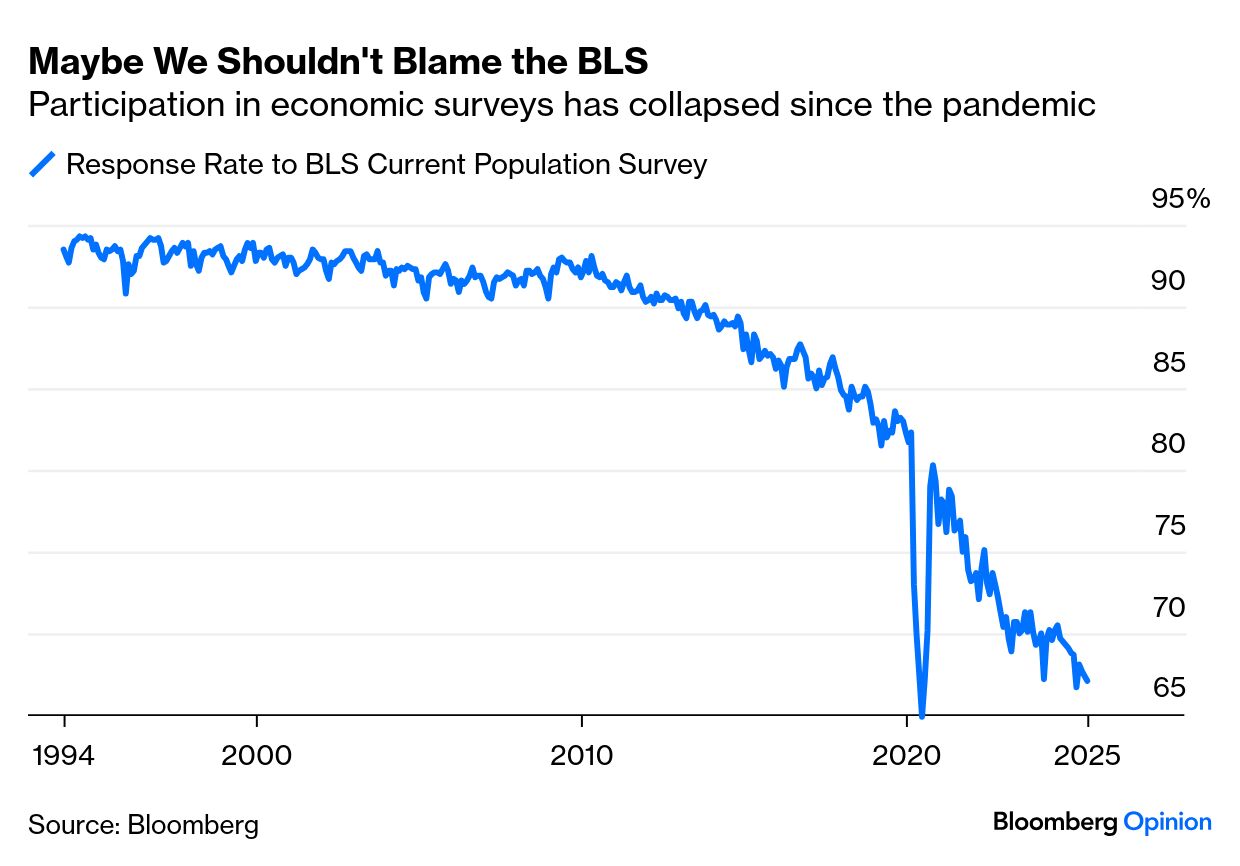

| It’s amazing how quickly momentum can reverse. The rally for risk assets had grown to look unstoppable since the US administration announced its first climbdown from the Liberation Day tariffs back in April. Nothing — not even a US attack on Iran or the reimposition of tariffs barely altered from the original plan — could stop stocks’ relentless outperformance. But for the second summer in a row, August has started with a dramatic reversal for stocks (proxied in the chart by the SPY exchange-traded fund) compared to bonds (proxied by the TLT ETF): Last year’s briefly terrifying reversal centered on Tokyo, and on a disappointing unemployment report. There was alarm at the triggering of the so-called Sahm Rule, named for Bloomberg Opinion colleague Claudia Sahm, which predicts a recession from how fast the unemployment rate has risen from its recent low. This time around, the Sahm Rule suggests a recession isn’t inevitable. Last year was a false alarm: This year’s August surprise started with disappointing jobs numbers, compounded by desultory supply manager surveys, and then by the news that the president was firing Erika McEntarfer, the head of the Bureau of Labor Statistics. News that the Fed Governor Adriana Kugler was resigning broke shortly before markets closed in New York — and this is significant, as it opens the chance to put the candidate Trump chooses as the next Fed chair on the board within weeks. That would weaken the incumbent, Jerome Powell, while also sowing confusion. This is how the news affected the dollar: Was this reaction justified? Probably. For months, the US labor market has seemed strangely resilient. Payrolls are still growing, but this latest report incorporated massive downward revisions to show the weakest jobs growth since 2011: That isn’t good for a multitude of reasons. It does, however, provide a clear justification to cut rates, as the president has been demanding. The problem is that inflation is picking up. The numbers are ambiguous but concerning. The Personal Consumption Expenditure deflator version of inflation, favored by the Fed, was released Thursday. Measuring it with the the Dallas Fed’s trimmed mean, favored by statisticians as a guide to underlying inflationary pressure, the direction is upward. Inflation never did return to the Fed’s 2% target: This probably isn’t enough to stop a rate cut in September, but it’s cause for concern. The ISM manufacturing report, which was poor, did at least provide the relative cheer that the prices paid by manufacturers dipped sharply compared to expectation. It remains elevated, but this does suggest that the slowing economy is counteracting inflationary pressure: All of this added up to the biggest one-day fall in the rate-sensitive two-year yield since the now little-remembered Powell Pivot at the December 2023 meeting of the Federal Open Market Committee — which appeared to promise imminent interest rate cuts, but didn’t. Earlier in the week, he had declined to make another such pivot, despite a couple of dissents from his colleagues. But with a data-dependent Fed, it is now a change in the numbers, rather than in the Fed’s words, that makes the difference: The shift in expectations for the Fed’s trajectory was clear-cut. After the employment numbers, the Bloomberg World Interest Rate Probabilities function shows that implicit expected fed funds rates were cut sharply. Futures see the rate below 3% by the end of next year: Last year’s August swoon was followed by a jumbo cut from the Fed, and soon swamped by excitement over an approaching Trump victory. Earnings resilience also helped. There’s a pretty good chance that happens again. There are two new risk factors this time. First, inflation is rising. Friday was also the day that the government, far from chickening out, unveiled steep new tariffs on the rest of the world. Markets are not priced for these things. Second, US credibility is now at issue. This is driven by the erratic way the government has dealt with tariffs and with its attempt to unseat Powell. The BLS news added another front. |