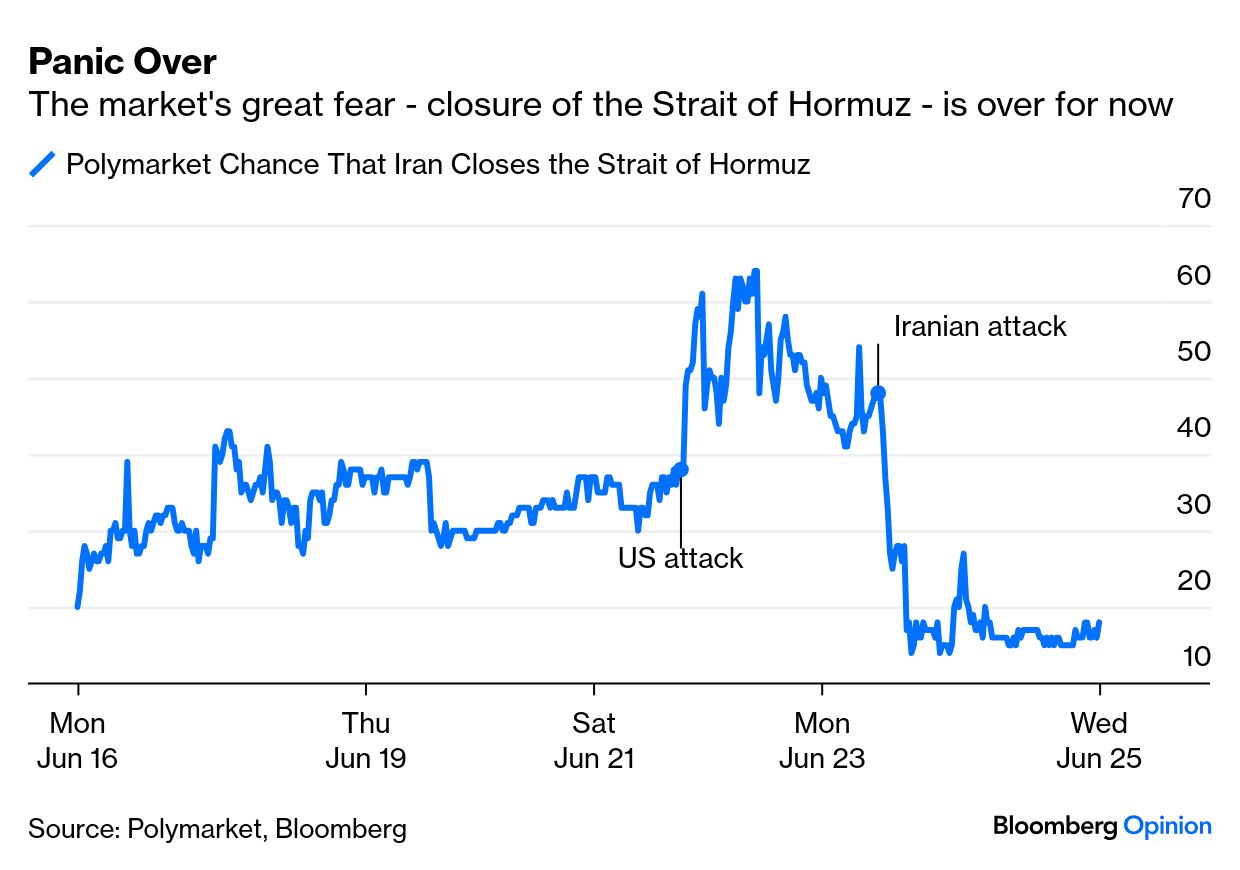

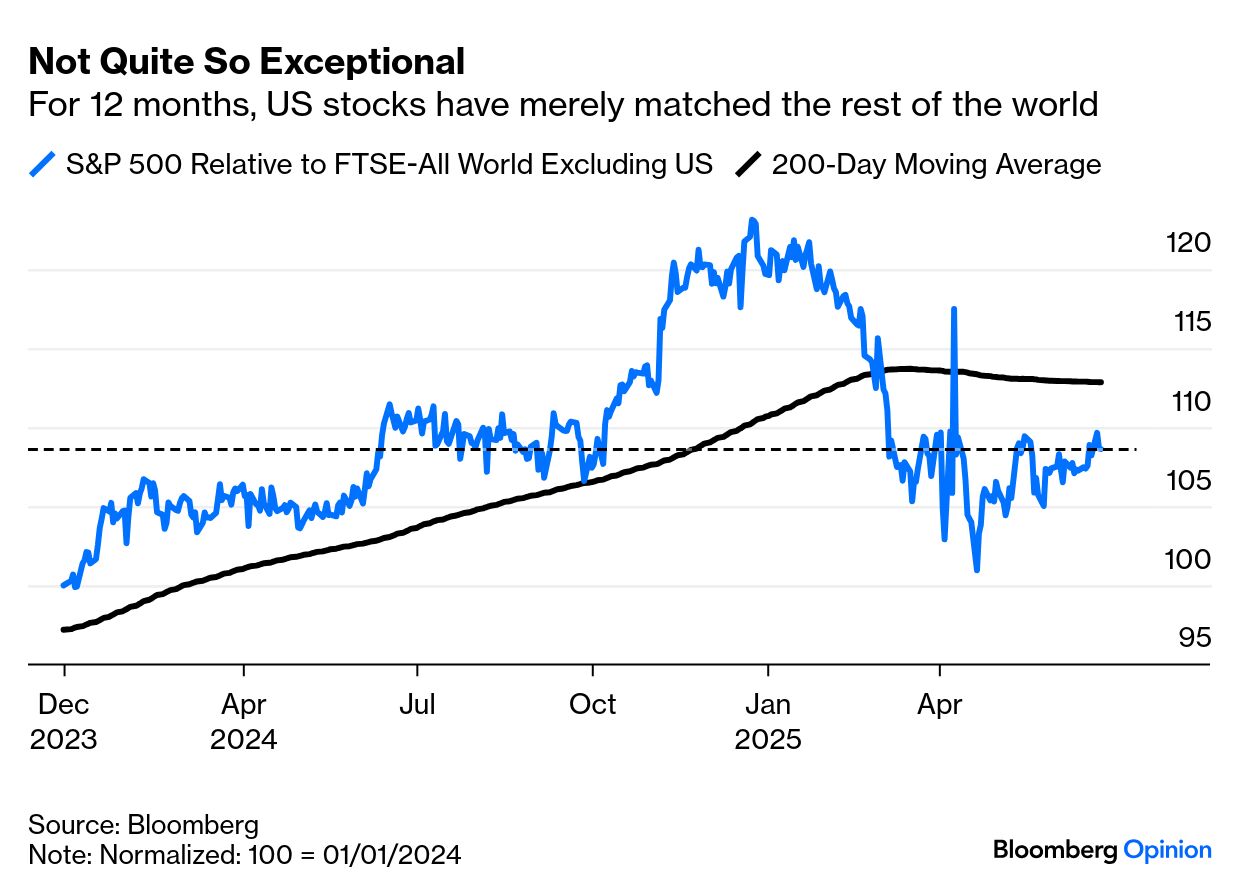

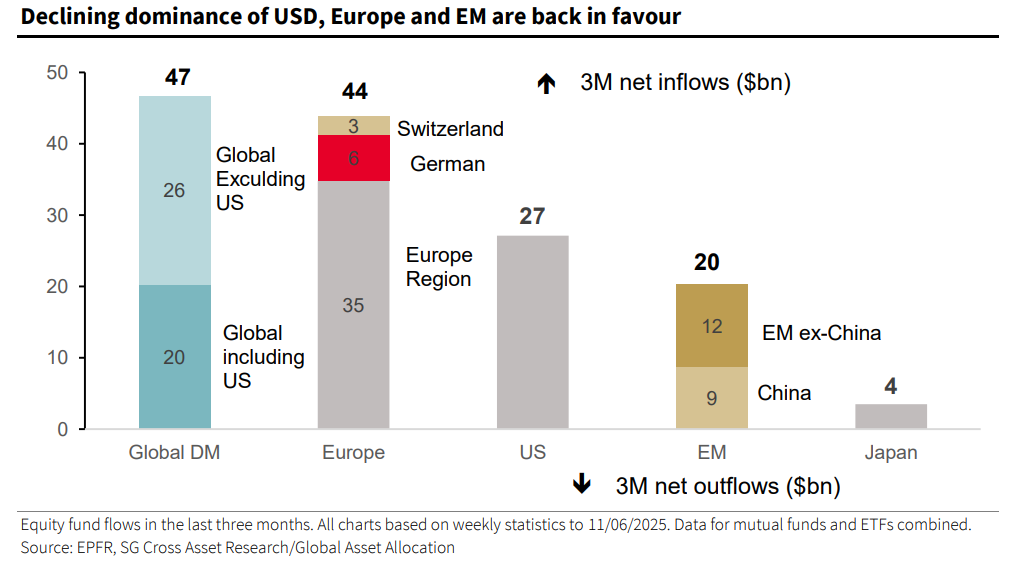

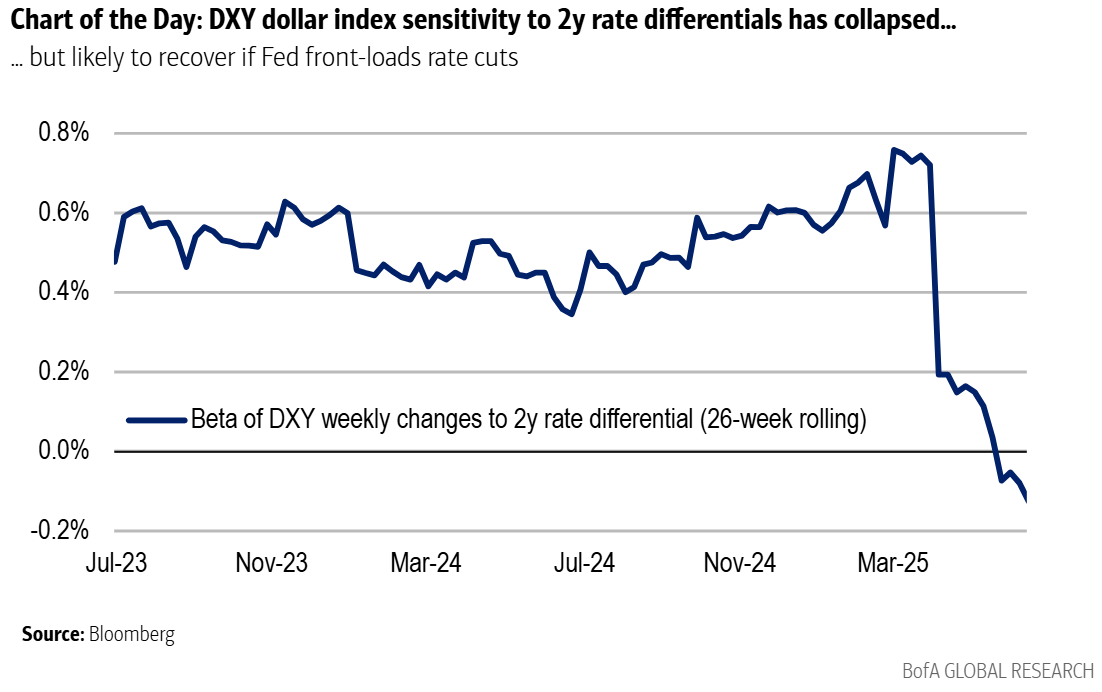

| Glad it’s all over? The conflagration in the Middle East, like all those that went before it, mattered chiefly to global markets if it threatened the supply of oil. Iran could, if it wanted, stop tankers from going through the Strait of Hormuz for a while. The perception that it might do so (at great cost to itself) reared after the US attacked Iranian nuclear facilities, and then dwindled when Iran’s limited response against a regional US air base showed that it wouldn’t go that far. This is how odds moved on the Polymarket prediction market: There’s room for argument about exactly how much damage the US has done to the Iranian nuclear project, but what matters for markets is that Tehran’s behavior makes clear that they aren’t going to close the Strait. As it’s hard to imagine a more obvious time, it lowers the odds they’d do so in the future. Hence, the oil supply is safe; this is what matters most to markets. Nobody thinks the long-running conflict has been resolved. Dangers very much remain. But the nuclear program is one of many geopolitical risks that have grumbled on in the background for years without affecting market valuations. Until the situation flares up again, the market can get back to ignoring Iran and its centrifuges. Make America Exceptional Again | The Israel-Iran ceasefire is a big political achievement for President Donald Trump. A more significant win, in economic terms, is his success in getting NATO allies to raise their defense spending. Not many would have seen that coming even a few months ago. There’s ample room to question the negotiating tactics he used, but they were effective. International markets are handing Trump 2.0 another victory. The S&P 500 is almost back to its record. Treasury Secretary Scott Bessent has targeted lower bond yields, cheaper oil, and a weaker dollar. The market is delivering all of them: Trump successes have led to a new idea. “Client questions recently reinforce our impression of a building narrative,” says Freya Beamish of TS Lombard. “Is the TACO [Trump Always Chickens Out] trade morphing into a reawakening of the US exceptionalism trade?” It’s questionable, however, whether American Exceptionalism — the relentless outperformance by US stocks — will resume after taking a break for the last few months. The most recent developments don’t help US outperformance. Cheaper oil is more important for European and Asia-Pacific economies than for the US, while the benefits of NATO members spending more on defense will likely flow primarily to European companies. And while the market trend has shown the US regaining ground, there’s no sign that investors are rethinking the judgment they made earlier this year that tariffs were a good reason to move elsewhere. In relative terms, the US has gained nothing since the eve of Liberation Day, April 2: Recent fund flows have helped Europe; this could continue. Societe Generale SA demonstrates that inflows to European funds actually exceeded those to the US over the last three months, while money has also gone into global funds that exclude the US. There are no flows out of the US as yet, so no particular reason to think that this trend cannot intensify. And in any case, as other markets are smaller, any investment into them will have greater proportionate impact: What hasn’t changed, at all, since Liberation Day and its subsequent reverses is the severing of the link between the dollar and its rate differentials. Normally, a currency will be aided by higher bond yields than are available elsewhere, as this will attract flows. That hasn’t happened this time. As this chart from Adarsh Sinha of Bank of America demonstrates, the relationship continues to weaken: The correlation could be restored if the Federal Reserve were to go through with cutting rates a little earlier than expected, and thus reduce rate differentials. “Earlier rate cuts by the Fed, whether accompanied by weaker data or not, would imply downside risk to our broader USD forecasts,” says Sinha. The context of cuts would matter. If the US labor market finally begins to crack, that would force the Fed to act and would weaken the dollar. Tariffs and the possibility that they raise inflation are causing the Fed to stay its hand for now — and again, if inflation does recur, that isn’t going to help the dollar. Further, the administration wants a weaker dollar. Washington is getting its way on military spending, and can probably get its way on this, too. If it were to pressure the Fed into cutting rates prematurely, that would weaken the dollar not only by lowering rate differentials, but also by harming the credibility of the central bank. Beamish suggests that the odds are stacked against the US, because “the probability that either the labor market cracks and/or the tariff effects show up in inflation” seems greater than “the probability that inflation continues to slow and the labor market holds up.” It’s best to assume that US exceptionalism will have to stay in abeyance a while longer. |