|

|

|

|

|

|

|

|

|

Home of the Week, 1546 Maryhill Rd., Woolwich, Ont. Kyle Christie/Kyle Christie

|

|

|

|

|

This week, we ask experts what they think about Prime Minister Mark Carney’s housing promises. Plus, COVID-era buyers sell at a loss, and one home worth a look. |

|

|

|

|

|

|

|

|

|

|

Will Carney end the housing crisis? The promise and peril of the Liberals’ plan |

|

|

|

|

|

|

|

|

|

|

|

|

|

The Liberals promised to increase housing supply by doubling the speed of construction to 500,000 new homes a year. DARRYL DYCK/The Canadian Press

|

|

|

|

|

Prime Minister Mark Carney and his Liberal minority government will have their work cut out for them as Canadians face the financial impacts of the trade war and ongoing cost-of-living concerns. And tackling the housing affordability crisis won’t get easier in this environment. |

|

|

|

|

During the campaign, the Liberals promised to increase housing supply by doubling the speed of construction to 500,000 new homes a year. To do that, the party pledged to create an entity called “Build Canada Homes,” that acts as a developer to oversee the construction of affordable housing. |

|

|

|

|

First-time homebuyers were also promised some relief, no longer having to pay GST on purchases of homes priced at or less than $1-million, and lower GST on homes between $1-million and $1.5-million. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

When exactly did Canadian housing become so unaffordable – and who’s to blame? |

|

|

|

|

|

|

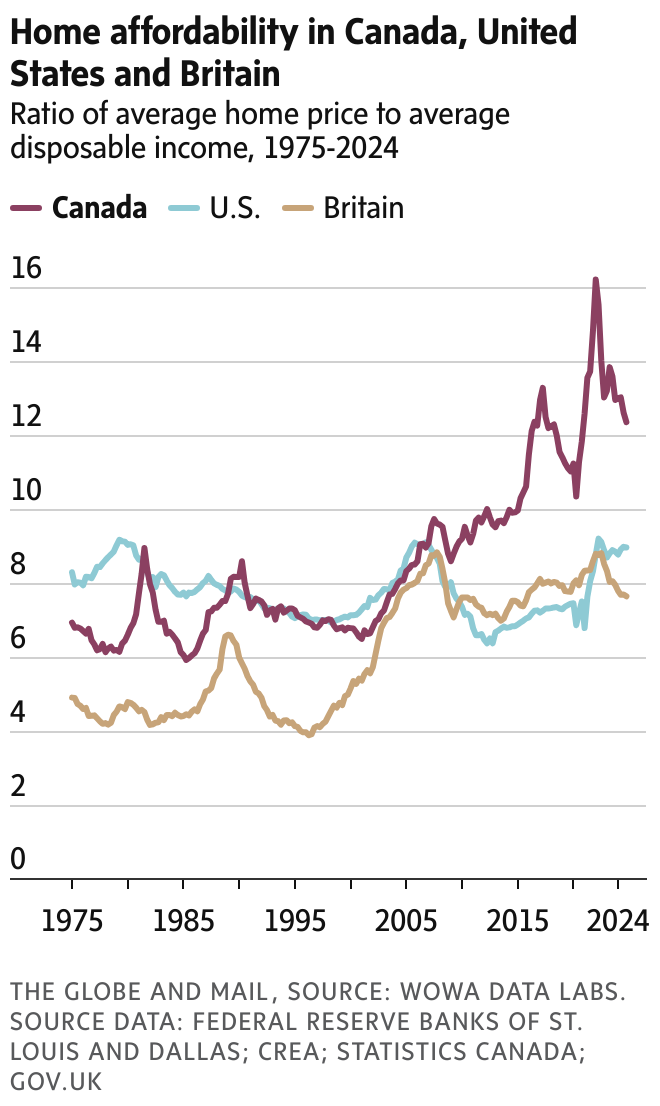

Home prices in Canada began rising steadily starting in 2001, but the true inflection point came around 2007 and 2008. Since then, the the ratio between home affordability and average disposable income has steadily rose, reaching a peak in 2022. So what changed in 2007-08? |

|

|

|

|

As Hanif Bayat writes, the primary factor that shifted the supply-demand balance toward unaffordability appears to be demand driven by speculative investment.

Ultralow interest rates made borrowing inexpensive and encouraged investors to use mortgage leverage for large returns on relatively small down payments. This led not only to worsening affordability, but Canadians now also carry the highest levels of personal debt in the top 10 world economies. |

|

|

|

|

|

|

|

|

|

|

Vancouver swamped by unsold condos as supply outpaces demand |

|

|

|

|

|

|

|

|

|

A condo tower under construction in downtown Vancouver, in February, 2020. DARRYL DYCK/The Canadian Press

|

|

|

|

|

Vancouver’s number of unsold, newly built condo units is expected to increase by 60 per cent by year’s end. As Kerry Gold writes, it’s a bleak situation for developers,

hampered by trade wars, an uncertain interest rate, rising costs and regulations designed to thwart a previous market that was driven by speculation and investment. Those days are over. One economist says the condo industry is currently “out of gas” as investors flee the housing market. |

|

|

|

|

This week’s lowest fixed and variable mortgage rates in Canada |

|

|

|

|

|

|

Rates shown are the lowest available for each term/type and category (insured versus uninsured) as of market close on Thursday May 1. |

|

|

|

|

|

|

|

|

|

|

In areas outside the GTA, homebuyers are wary |

|

|

|

|

Real estate agents say move-up buyers in cities around Ontario’s Greater Golden Horseshoe are rare and first-time purchasers are wary. As Carolyn Ireland writes, weakening labour markets and U.S. tariffs are still souring market activity. As for whether the end of the federal election will encourage more buyers to come out of the woodwork, Ireland told me it’s too soon to tell. |

|

|

|

|

“Certainly agents hope it will remove one element of uncertainty but we don’t know yet if their wishes will come true,” she said. “There are just so many other, bigger unknowns.” |

|

|

|

|

|

|

|

|

|

|

In Ontario, selling at a loss becomes commonplace |

|

|

|

|

|

|

|

|

|

Real estate for sale signs are shown in Oakville, Ont. in December, 2018. Richard Buchan/The Canadian Press

|

|

|